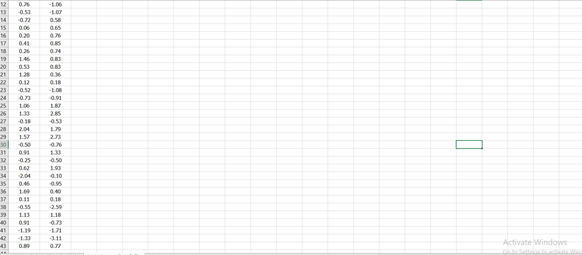

Question

Consider the daily percent change in the stock price of two companies, A and B, in an investment portfolio. The dataset is called Investment Portfolio.

Consider the daily percent change in the stock price of two companies, A and B, in an

investment portfolio. The dataset is called Investment Portfolio.

Answer the following questions manually. Use statistical software or MS Excel for help with

the computation of any summary statistics needed for manual computations.

a) Draw a scatterplot of the company A daily percent changes against the company B daily

percent changes. Describe the relationship between daily percent changes that you see

in this scatterplot.

b) Determine the regression equation to predict the daily percent change in the stock price

of company A from the daily percent change in the stock price of company B. Interpret

the value of the slope coefficient.

c) Find the correlation between the percent changes. Does the correlation value support

your description of the scatterplot in part a)?

d) Compute the corresponding coefficient of determination and interpret its value. In

financial terms, it represents the proportion of non-diversifiable risk in company A.

e) Compute the 95% confidence interval for the slope coefficient.

f) Test at the 5% significance level whether the slope coefficient is significantly different

from 1, representing the beta of a highly diversified portfolio. Don't forget to show your

computations.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Algebra

Authors: Marvin L Bittinger

11th Edition

0321968395, 9780321968395