Answered step by step

Verified Expert Solution

Question

1 Approved Answer

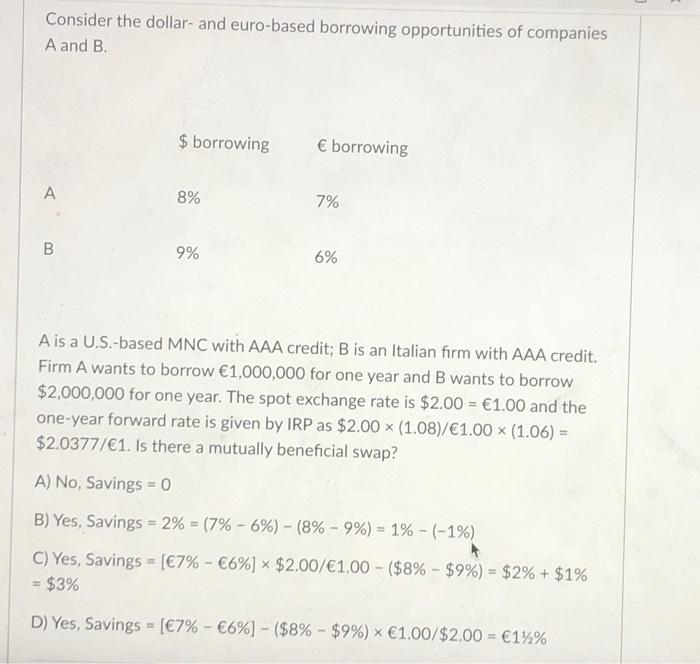

Consider the dollar- and euro-based borrowing opportunities of companies A and B. A B $ borrowing borrowing 8% 9% 7% 6% A is a U.S.-based

Consider the dollar- and euro-based borrowing opportunities of companies A and B. A B $ borrowing borrowing 8% 9% 7% 6% A is a U.S.-based MNC with AAA credit; B is an Italian firm with AAA credit. Firm A wants to borrow 1,000,000 for one year and B wants to borrow $2,000,000 for one year. The spot exchange rate is $2.00 = 1.00 and the one-year forward rate is given by IRP as $2.00 x (1.08) / 1.00 (1.06) = $2.0377/1. Is there a mutually beneficial swap? A) No, Savings = 0 B) Yes, Savings = 2% = (7% -6%) - (8% -9%) = 1% - (-1%) C) Yes, Savings = [7% - 6%] $2.00/1.00 - ($8% - $9%) = $2% + $1% = $3% D) Yes, Savings = [7% - 6%] - ($8% - $9%) 1.00/$2.00 = 1%% More

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Asset Management And Institutional Investors

Authors: Ignazio Basile, Pierpaolo Ferrari

1st Edition

331932795X,3319327968