Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Consider the following. a . Calculate the leverage - adjusted duration gap of an F I that has assets of $ 2 . 2 million

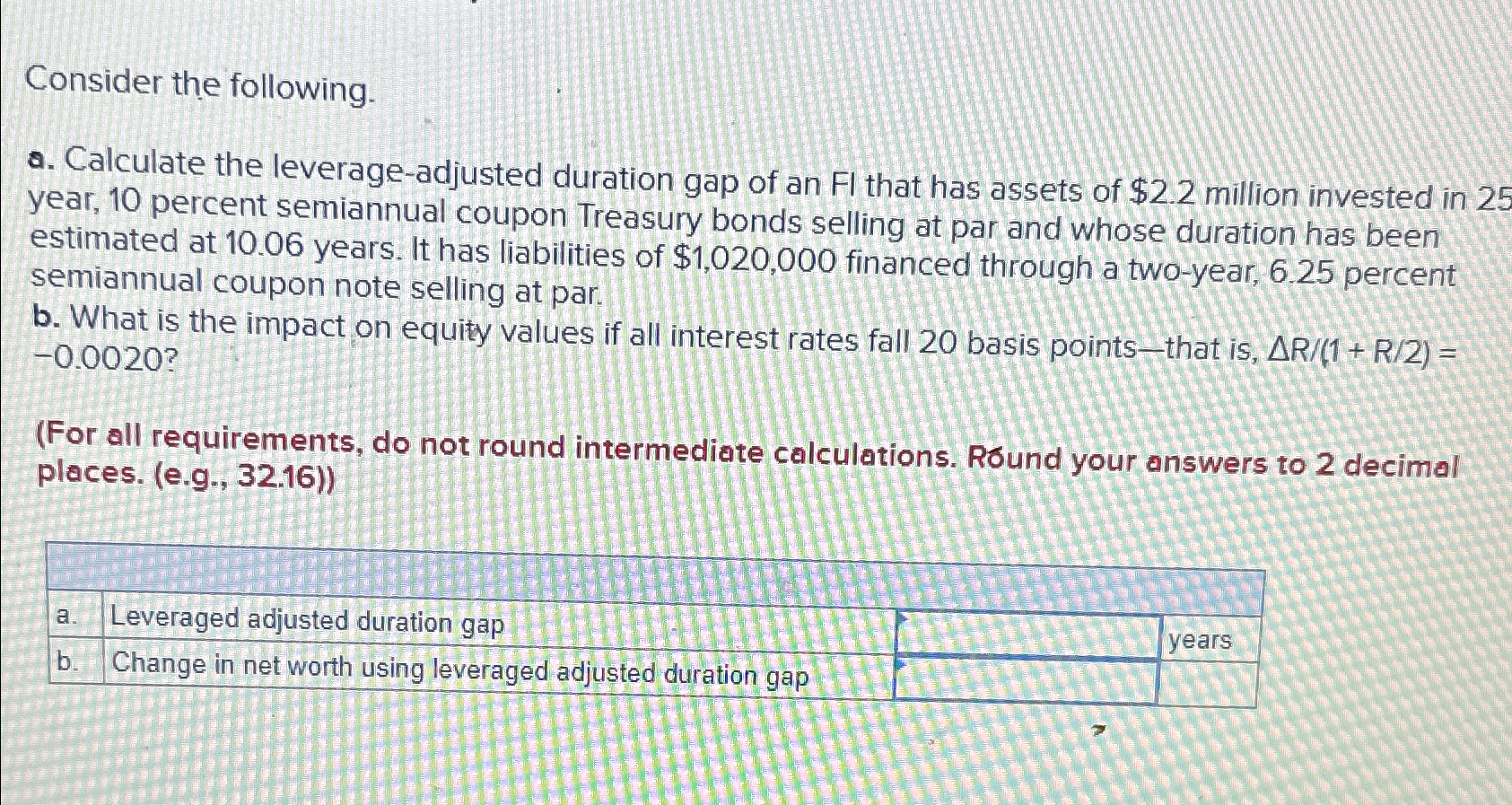

Consider the following.

a Calculate the leverageadjusted duration gap of an that has assets of $ million invested in year, percent semiannual coupon Treasury bonds selling at par and whose duration has been estimated at years. It has liabilities of $ financed through a twoyear, percent semiannual coupon note selling at par.

b What is the impact on equity values if all interest rates fall basis points that is

For all requirements, do not round intermediate calculations. Round your answers to decimal places. eg

tableaLeveraged adjusted duration gap,,yearsbChange in net worth using leveraged adjusted duration gap,,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment Science

Authors: David G. Luenberger

1st International Edition

0195391063, 9780195391060