Answered step by step

Verified Expert Solution

Question

1 Approved Answer

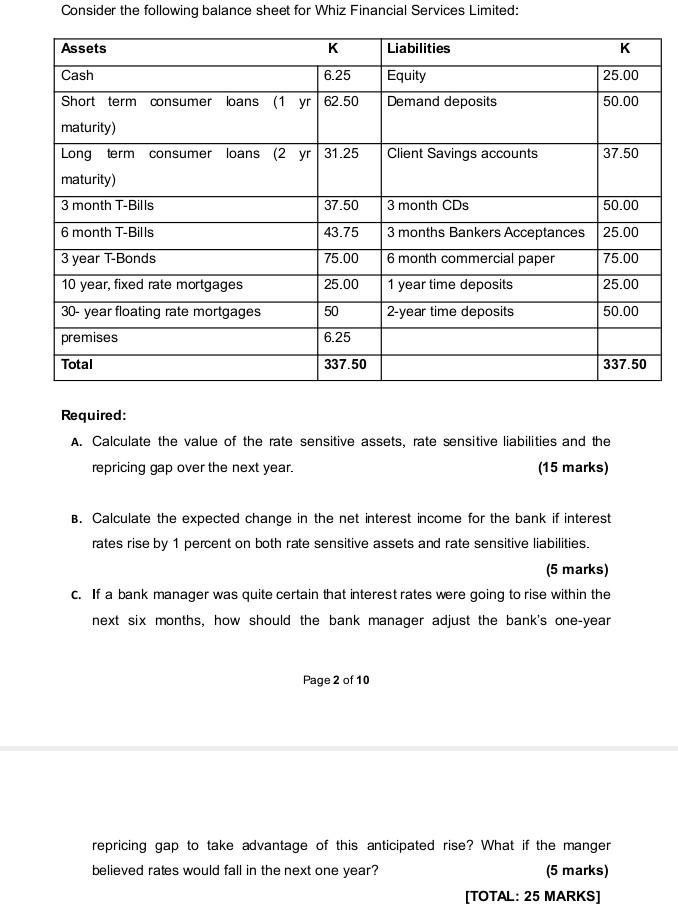

Consider the following balance sheet for Whiz Financial Services Limited: Required: A. Calculate the value of the rate sensitive assets, rate sensitive liabilities and the

Consider the following balance sheet for Whiz Financial Services Limited: Required: A. Calculate the value of the rate sensitive assets, rate sensitive liabilities and the repricing gap over the next year. (15 marks) B. Calculate the expected change in the net interest income for the bank if interest rates rise by 1 percent on both rate sensitive assets and rate sensitive liabilities. (5 marks) c. If a bank manager was quite certain that interest rates were going to rise within the next six months, how should the bank manager adjust the bank's one-year Page 2 of 10 repricing gap to take advantage of this anticipated rise? What if the manger believed rates would fall in the next one year? (5 marks) [TOTAL: 25 MARKS]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Supply Chain Finance Solutions

Authors: Erik Hofmann, Oliver Belin

1st Edition

3642175651, 978-3642175657