Answered step by step

Verified Expert Solution

Question

1 Approved Answer

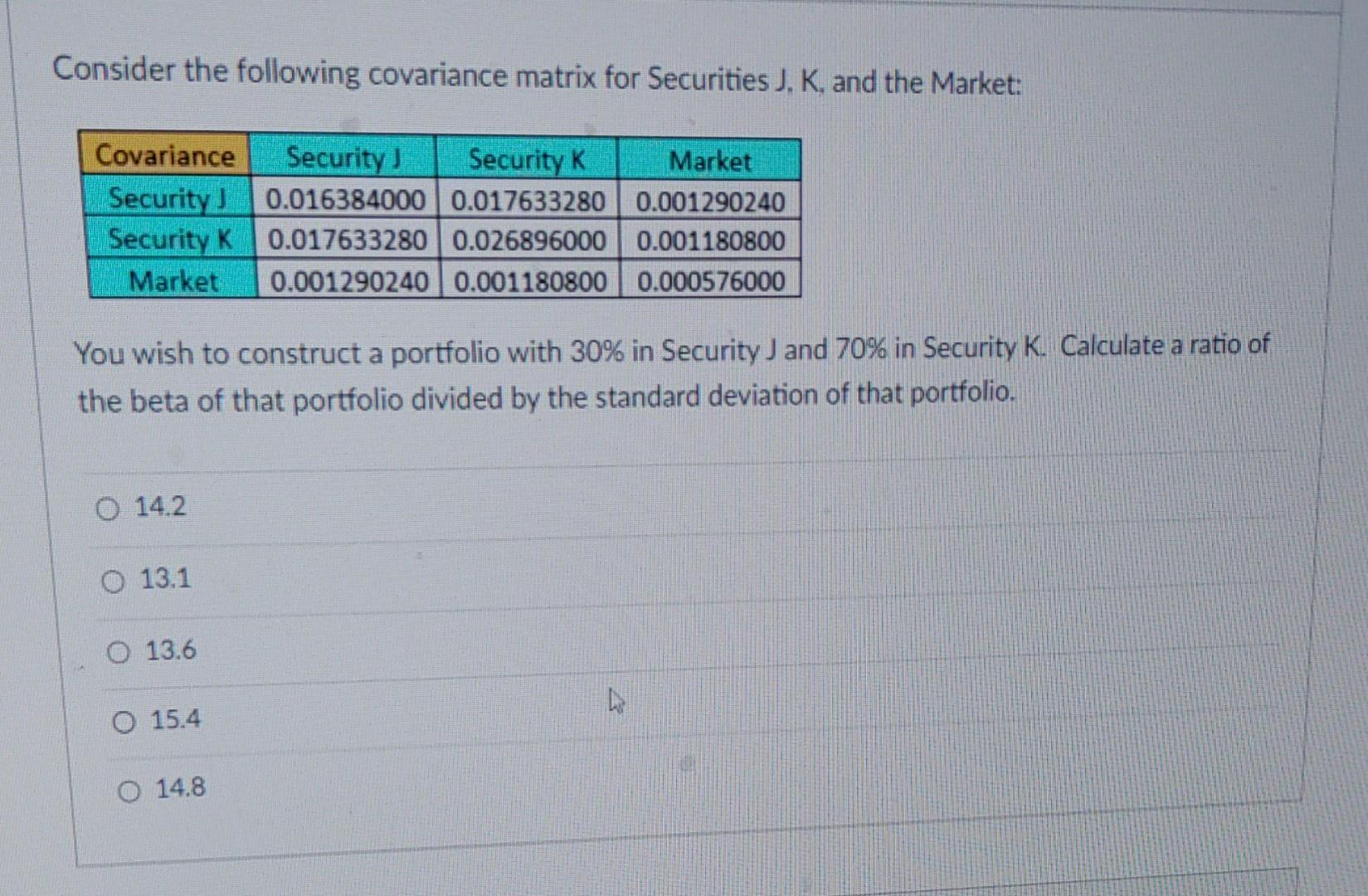

Consider the following covariance matrix for Securities J, K, and the Market: You wish to construct a portfolio with 30% in Security J and 70%

Consider the following covariance matrix for Securities J, K, and the Market: You wish to construct a portfolio with 30% in Security J and 70% in Security K. Calculate a ratio of the beta of that portfolio divided by the standard deviation of that portfolio. 14.2 13.1 13.6 15.4 14.8

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Economics Discussion Series The Relocation Decisions Of Working Couples

Authors: United States Federal Reserve Board, Jonathan F. Pingle

1st Edition

1288709137, 9781288709137