Answered step by step

Verified Expert Solution

Question

1 Approved Answer

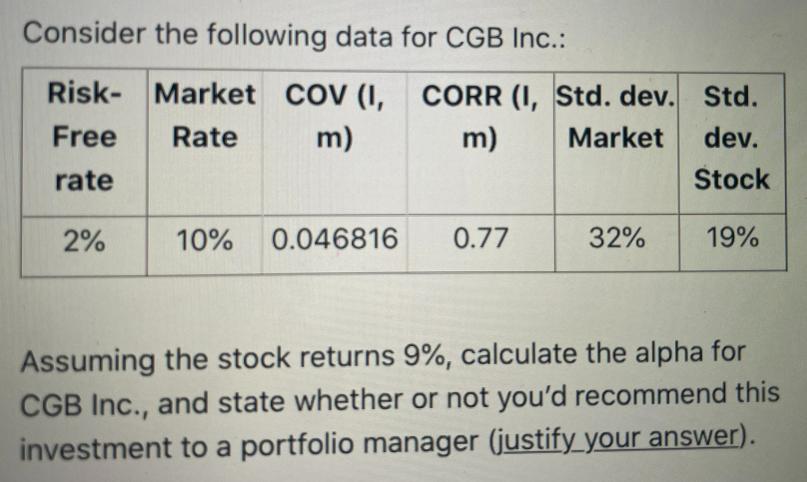

Consider the following data for CGB Inc.: Risk- Market COV (I, Rate m) Free rate 2% 10% 0.046816 CORR (I, Std. dev. Std. Market

Consider the following data for CGB Inc.: Risk- Market COV (I, Rate m) Free rate 2% 10% 0.046816 CORR (I, Std. dev. Std. Market m) dev. Stock 19% 0.77 32% Assuming the stock returns 9%, calculate the alpha for CGB Inc., and state whether or not you'd recommend this investment to a portfolio manager (justify your answer).

Step by Step Solution

★★★★★

3.43 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the alpha for CGB Inc we need to use the Capital Asset Pricing Model CAPM formula Alpha ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516