Question

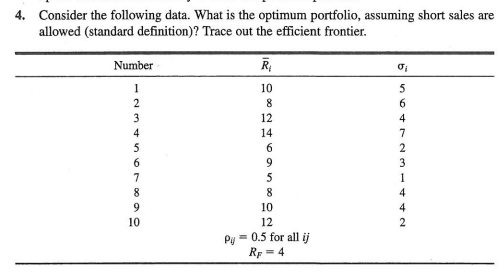

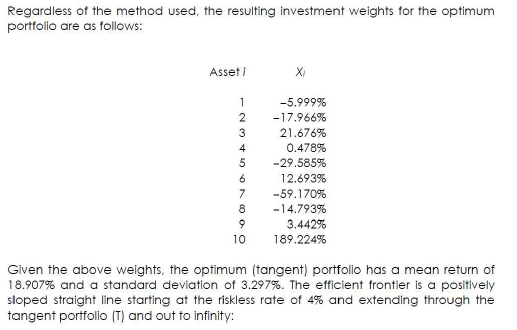

Consider the following data. What is the optimum portfolio, assuming short sales are allowed (standard definition)? Trace out the efficient frontier. Below are the answers

Consider the following data. What is the optimum portfolio, assuming short sales are allowed (standard definition)? Trace out the efficient frontier.

Below are the answers provided by my lecturer, I want to know how he got to these answers.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture capital and the finance of innovation

Authors: Andrew Metrick

2nd Edition

9781118137888, 470454709, 1118137884, 978-0470454701