Answered step by step

Verified Expert Solution

Question

1 Approved Answer

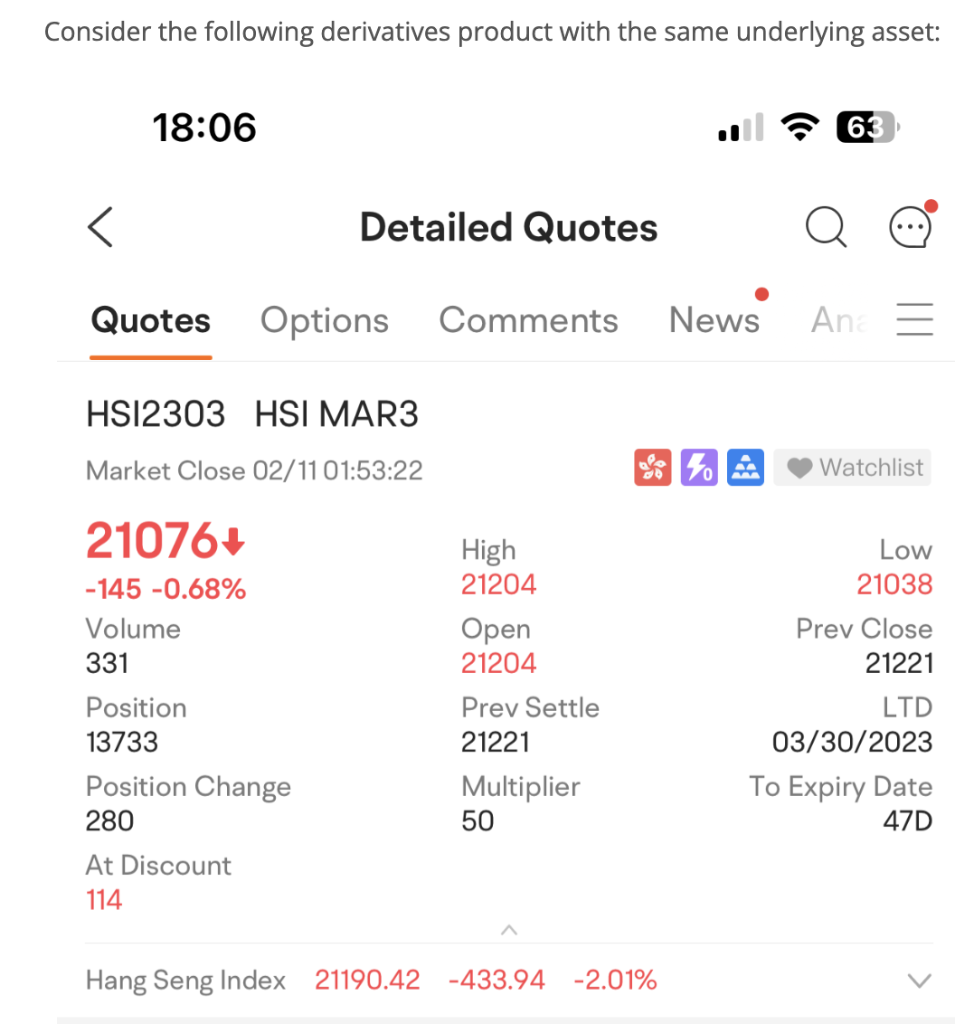

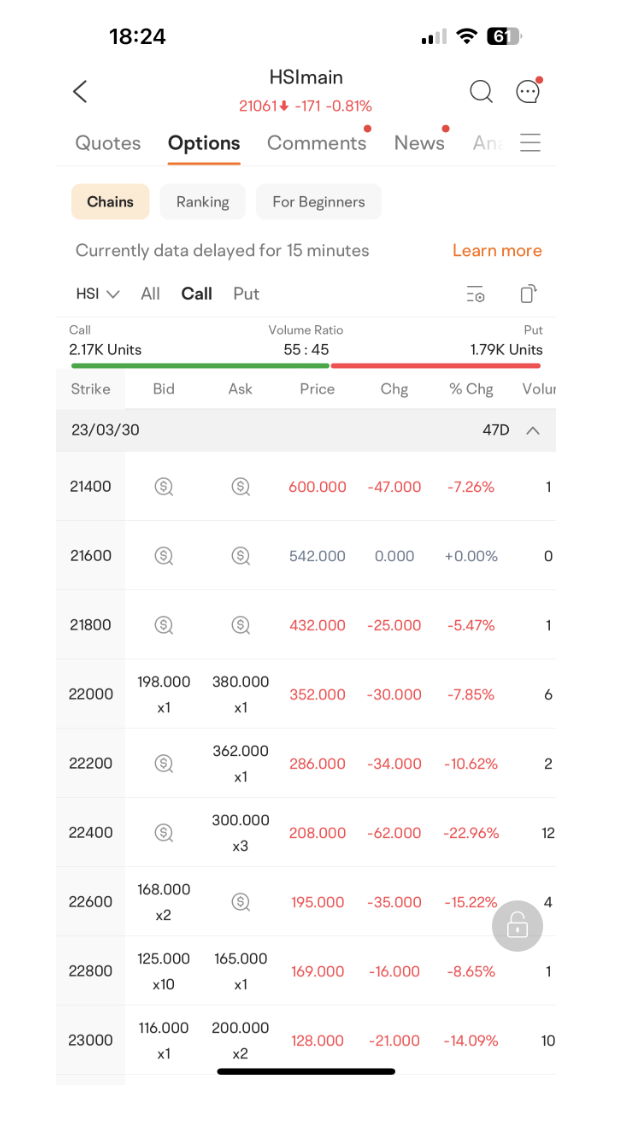

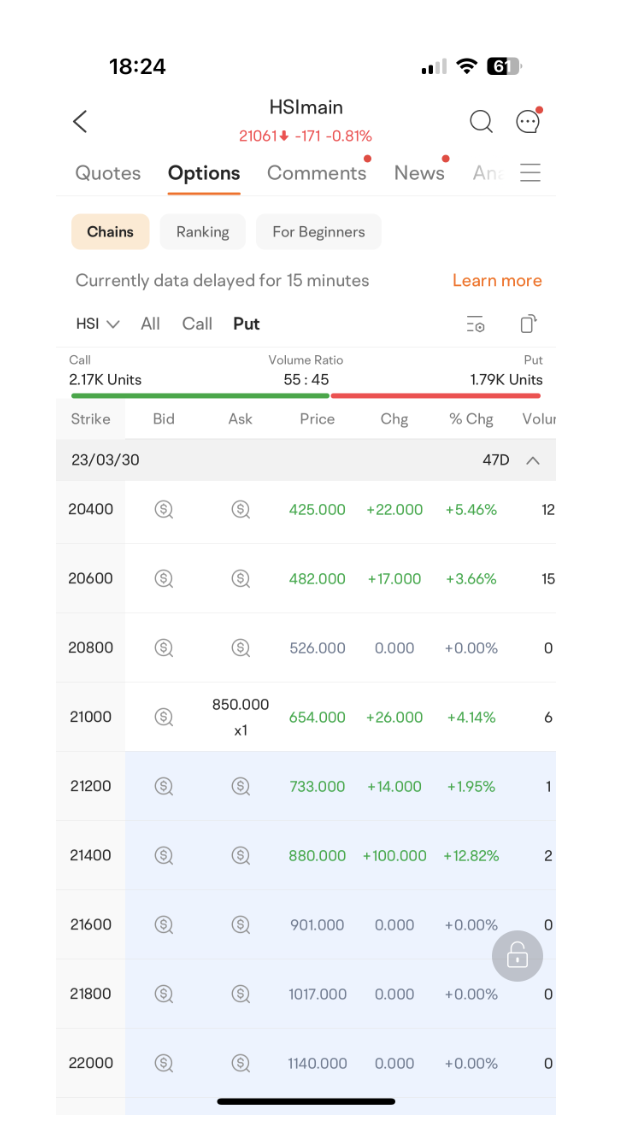

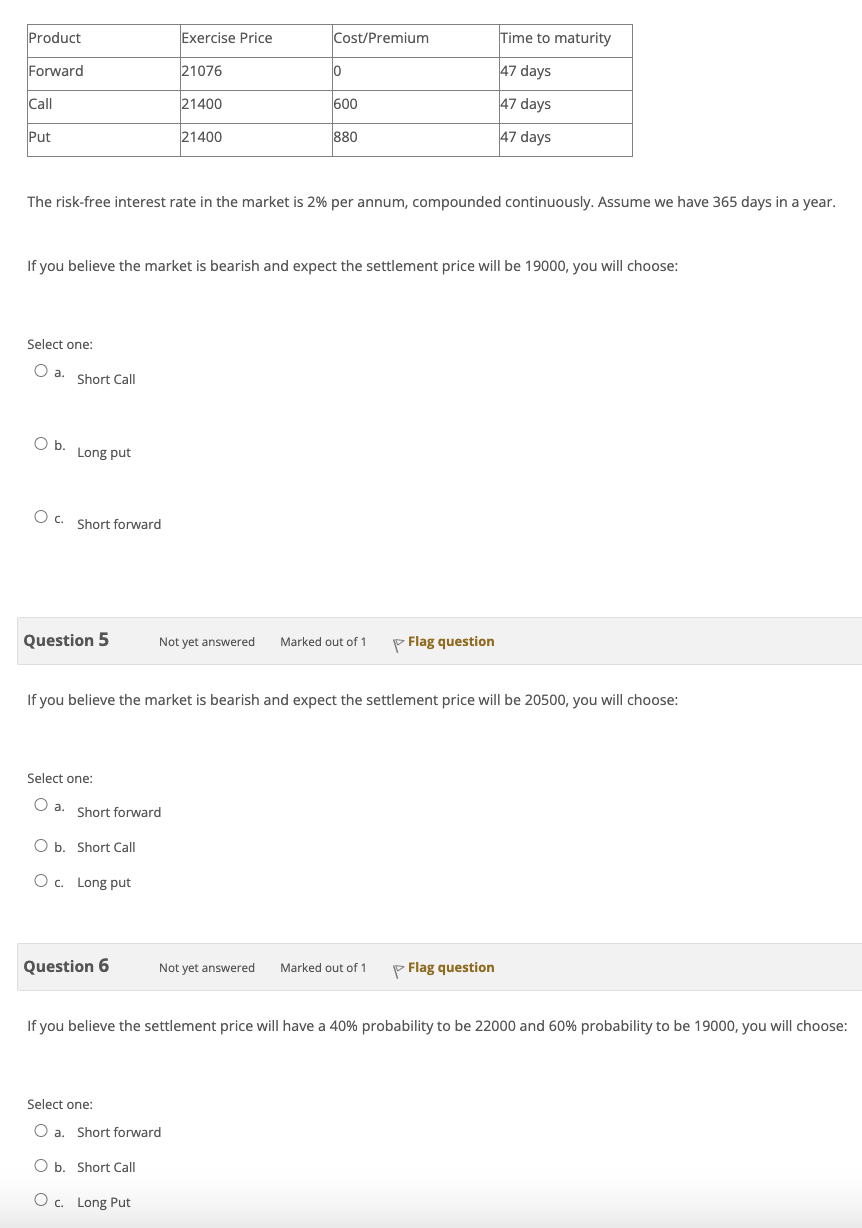

Consider the following derivatives product with the same underlying asset: 3m= 18:24 61 21400 ($) ($) 600.00047.0007.26% 1 21600 ($) ($) 542.0000.000+0.00%0 18:24 (1) 61

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fatal Numbers Why Count On Chance

Authors: Hans Magnus Enzensberger ,Karen Leeder

1st Edition

1935830015, 978-1935830016