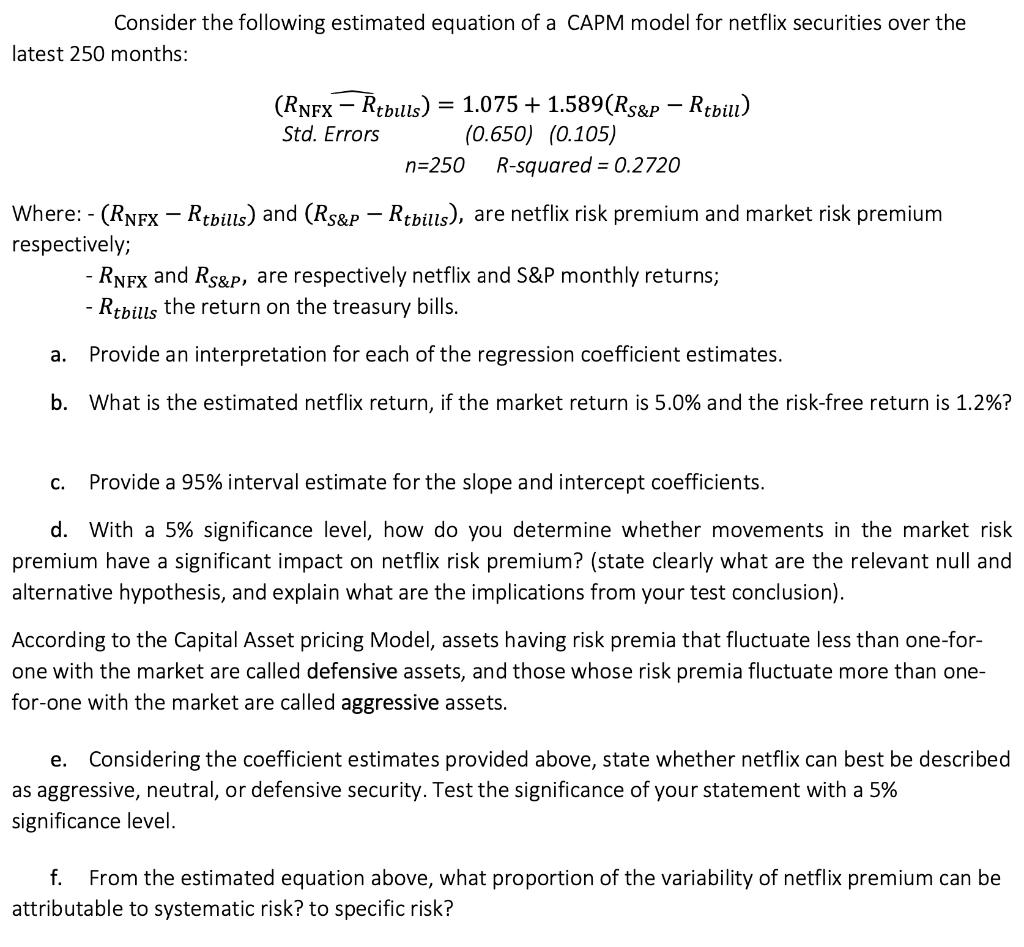

Consider the following estimated equation of a CAPM model for netflix securities over the latest 250 months: (RNFX - Rtbills) = 1.075 + 1.589(Rs&p Rtbill) Std. Errors (0.650) (0.105) n=250 R-squared = 0.2720 Where: - (RNEX Rtbills) and (Rs&p - Rtbills), are netflix risk premium and market risk premium respectively; - RNFx and Rs&p, are respectively netflix and S&P monthly returns; - Rtbills the return on the treasury bills. a. Provide an interpretation for each of the regression coefficient estimates. b. What is the estimated netflix return, if the market return is 5.0% and the risk-free return is 1.2%? C. Provide a 95% interval estimate for the slope and intercept coefficients. d. With a 5% significance level, how do you determine whether movements in the market risk premium have a significant impact on netflix risk premium? (state clearly what are the relevant null and alternative hypothesis, and explain what are the implications from your test conclusion). According to the Capital Asset pricing Model, assets having risk premia that fluctuate less than one-for- one with the market are called defensive assets, and those whose risk premia fluctuate more than one- for-one with the market are called aggressive assets. e. Considering the coefficient estimates provided above, state whether netflix can best be described as aggressive, neutral, or defensive security. Test the significance of your statement with a 5% significance level. f. From the estimated equation above, what proportion of the variability of netflix premium can be attributable to systematic risk? to specific risk? Consider the following estimated equation of a CAPM model for netflix securities over the latest 250 months: (RNFX - Rtbills) = 1.075 + 1.589(Rs&p Rtbill) Std. Errors (0.650) (0.105) n=250 R-squared = 0.2720 Where: - (RNEX Rtbills) and (Rs&p - Rtbills), are netflix risk premium and market risk premium respectively; - RNFx and Rs&p, are respectively netflix and S&P monthly returns; - Rtbills the return on the treasury bills. a. Provide an interpretation for each of the regression coefficient estimates. b. What is the estimated netflix return, if the market return is 5.0% and the risk-free return is 1.2%? C. Provide a 95% interval estimate for the slope and intercept coefficients. d. With a 5% significance level, how do you determine whether movements in the market risk premium have a significant impact on netflix risk premium? (state clearly what are the relevant null and alternative hypothesis, and explain what are the implications from your test conclusion). According to the Capital Asset pricing Model, assets having risk premia that fluctuate less than one-for- one with the market are called defensive assets, and those whose risk premia fluctuate more than one- for-one with the market are called aggressive assets. e. Considering the coefficient estimates provided above, state whether netflix can best be described as aggressive, neutral, or defensive security. Test the significance of your statement with a 5% significance level. f. From the estimated equation above, what proportion of the variability of netflix premium can be attributable to systematic risk? to specific risk