Answered step by step

Verified Expert Solution

Question

1 Approved Answer

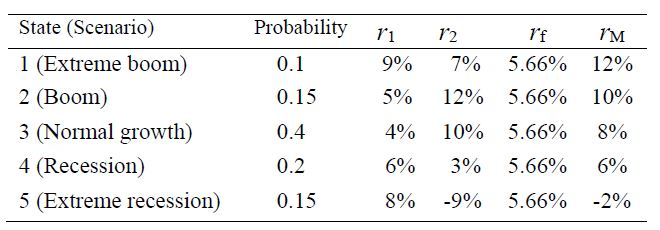

Consider the following forecasts of returns on two risky assets (r 1 and r2), risk-free asset (r f ), and the market (r M ):

Consider the following forecasts of returns on two risky assets (r1 and r2), risk-free asset (rf), and the market (rM):

Compute the expected returns, standard deviations for both securities (E(r1), 1, E(r2), and 2)1 and the market (E(rM) and M), as well as 1 and 2.

Probability T12 State (Scenario) 1 (Extreme boom) 2 (Boom) 3 (Normal growth) 4 (Recession) 5 (Extreme recession)0.15 0.1 0.15 0.4 0.2 9% 5% 4% 6% 8% 7% 12% 10% 300 -9% If 5.66% 5.66% 5.66% 5.66% 5.66% TM 12% 10% 8% 6% -2%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started