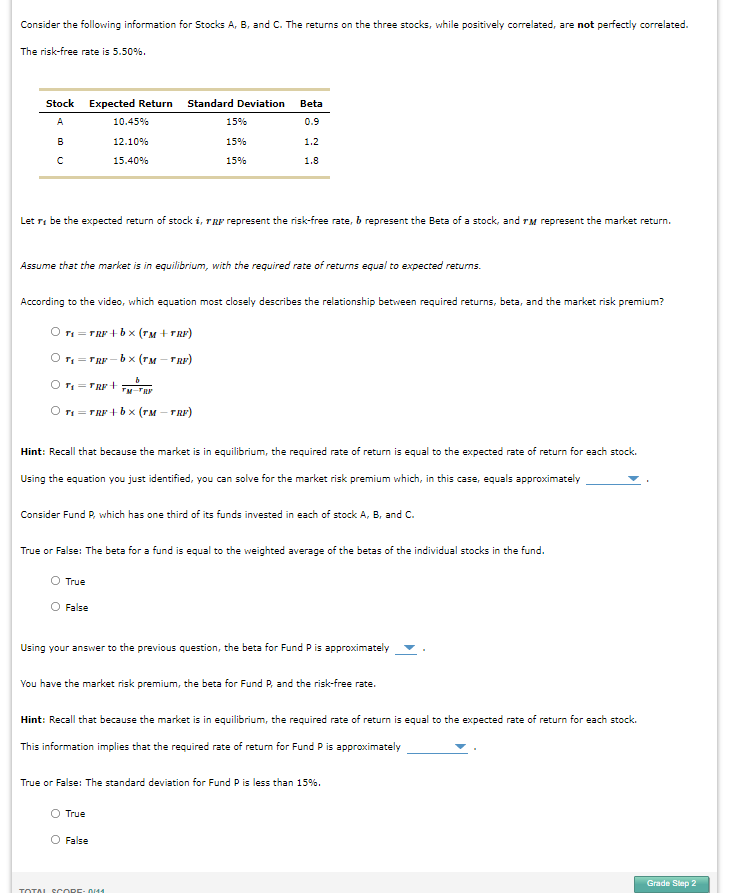

Consider the following information for Stocks A, B, and C. The returns on the three stocks, while positively correlated, are not perfectly correlated. The risk-free rate is 5.50%. Stock Expected Return Standard Deviation Beta A 10.45% 15% 0.9 B 12.10% 15% 1.2 15.40% 15% 1.8 Letr, be the expected return of stock i, TRP represent the risk-free rate, b represent the Beta of a stock, and TM represent the market return. Assume that the market is in equilibrium, with the required rate of returns equal to expected returns. According to the video, which equation most closely describes the relationship between required returns, beta, and the market risk premium? OT=TRF+bx (TM+TRF) OT=TRF-bx (TM-TRF) b OT=TRE+ TM-TRY T=TRF+bx (TM-TRF) Hint: Recall that because the market is in equilibrium, the required rate of return is equal to the expected rate of return for each stock. Using the equation you just identified, you can solve for the market risk premium which, in this case, equals approximately Consider Fund P, which has one third of its funds invested in each of stock A, B, and C. True or False: The beta for a fund is equal to the weighted average of the betas of the individual stocks in the fund. True O False Using your answer to the previous question, the beta for Fund P is approximately You have the market risk premium, the beta for Fund P, and the risk-free rate. Hint: Recall that because the market is in equilibrium, the required rate of return is equal to the expected rate of return for each stock. This information implies that the required rate of return for Fund P is approximately True or False: The standard deviation for Fund P is less than 15%. O True O False Grade Step 2 TOTAL SCORE: 0111 Consider the following information for Stocks A, B, and C. The returns on the three stocks, while positively correlated, are not perfectly correlated. The risk-free rate is 5.50%. Stock Expected Return Standard Deviation Beta A 10.45% 15% 0.9 B 12.10% 15% 1.2 15.40% 15% 1.8 Letr, be the expected return of stock i, TRP represent the risk-free rate, b represent the Beta of a stock, and TM represent the market return. Assume that the market is in equilibrium, with the required rate of returns equal to expected returns. According to the video, which equation most closely describes the relationship between required returns, beta, and the market risk premium? OT=TRF+bx (TM+TRF) OT=TRF-bx (TM-TRF) b OT=TRE+ TM-TRY T=TRF+bx (TM-TRF) Hint: Recall that because the market is in equilibrium, the required rate of return is equal to the expected rate of return for each stock. Using the equation you just identified, you can solve for the market risk premium which, in this case, equals approximately Consider Fund P, which has one third of its funds invested in each of stock A, B, and C. True or False: The beta for a fund is equal to the weighted average of the betas of the individual stocks in the fund. True O False Using your answer to the previous question, the beta for Fund P is approximately You have the market risk premium, the beta for Fund P, and the risk-free rate. Hint: Recall that because the market is in equilibrium, the required rate of return is equal to the expected rate of return for each stock. This information implies that the required rate of return for Fund P is approximately True or False: The standard deviation for Fund P is less than 15%. O True O False Grade Step 2 TOTAL SCORE: 0111