Answered step by step

Verified Expert Solution

Question

1 Approved Answer

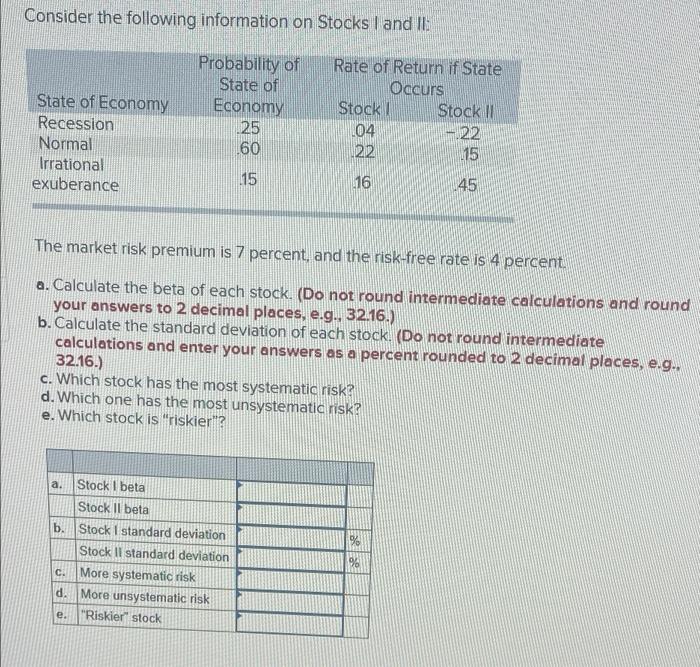

Consider the following information on Stocks I and II Probability of State of Economy 25 State of Economy Recession Normal Irrational exuberance Rate of Return

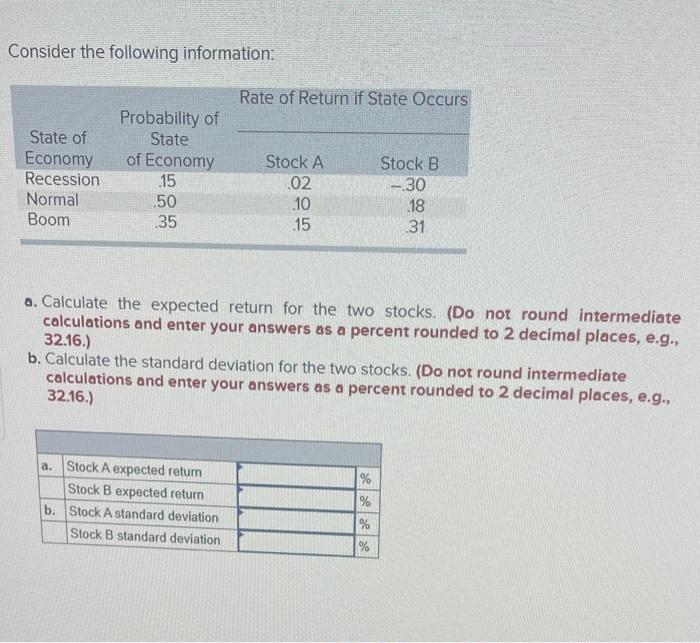

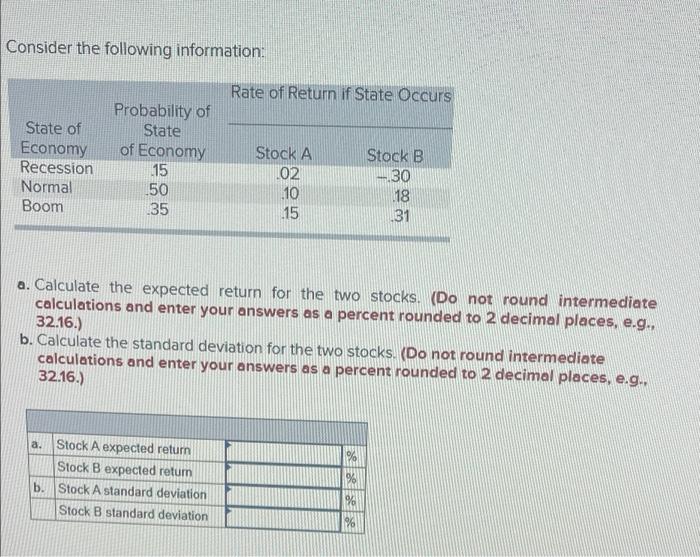

Consider the following information on Stocks I and II Probability of State of Economy 25 State of Economy Recession Normal Irrational exuberance Rate of Return if State Occurs Stock Stock Il 04 - 22 22 60 1.15 16 45 The market risk premium is 7 percent, and the risk-free rate is 4 percent a. Calculate the beta of each stock. (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) b. Calculate the standard deviation of each stock. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g.. 32.16.) c. Which stock has the most systematic risk? d. Which one has the most unsystematic risk e. Which stock is "riskier"? a. Stock I beta Stock Il beta b. Stock i standard deviation Stock Il standard deviation c. More systematic risk d. More unsystematic risk e. "Riskier" stock 9 Consider the following information: Rate of Return if State Occurs State of Economy Recession Normal Boom Probability of State of Economy .15 50 .35 Stock A 02 .10 .15 Stock B --30 18 .31 a. Calculate the expected return for the two stocks. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) b. Calculate the standard deviation for the two stocks. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) a. Stock A expected retum Stock B expected return b. Stock A standard deviation Stock B standard deviation % % de les % % Consider the following information: Rate of Return if State Occurs State of Economy Recession Normal Boom Probability of State of Economy 15 150 135 Stock A L02 10 15 Stock B - 30 .18 31 a. Calculate the expected return for the two stocks. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g.. 32.16.) b. Calculate the standard deviation for the two stocks. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g.. 32.16.) a. Stock A expected return Stock B expected retum b. Stock A standard deviation Stock B standard deviation 9 96

Consider the following information on Stocks I and II Probability of State of Economy 25 State of Economy Recession Normal Irrational exuberance Rate of Return if State Occurs Stock Stock Il 04 - 22 22 60 1.15 16 45 The market risk premium is 7 percent, and the risk-free rate is 4 percent a. Calculate the beta of each stock. (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) b. Calculate the standard deviation of each stock. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g.. 32.16.) c. Which stock has the most systematic risk? d. Which one has the most unsystematic risk e. Which stock is "riskier"? a. Stock I beta Stock Il beta b. Stock i standard deviation Stock Il standard deviation c. More systematic risk d. More unsystematic risk e. "Riskier" stock 9 Consider the following information: Rate of Return if State Occurs State of Economy Recession Normal Boom Probability of State of Economy .15 50 .35 Stock A 02 .10 .15 Stock B --30 18 .31 a. Calculate the expected return for the two stocks. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) b. Calculate the standard deviation for the two stocks. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) a. Stock A expected retum Stock B expected return b. Stock A standard deviation Stock B standard deviation % % de les % % Consider the following information: Rate of Return if State Occurs State of Economy Recession Normal Boom Probability of State of Economy 15 150 135 Stock A L02 10 15 Stock B - 30 .18 31 a. Calculate the expected return for the two stocks. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g.. 32.16.) b. Calculate the standard deviation for the two stocks. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g.. 32.16.) a. Stock A expected return Stock B expected retum b. Stock A standard deviation Stock B standard deviation 9 96

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Globalization Gating And Risk Finance

Authors: Unurjargal Nyambuu, Charles S. Tapiero

1st Edition

1119252652, 978-1119252658