Answered step by step

Verified Expert Solution

Question

1 Approved Answer

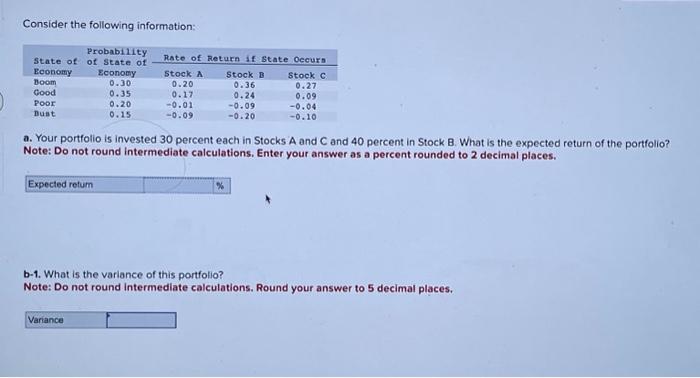

Consider the following information: Probability State of of State of Economy Boom Good Poor Bust Expected return Economy 0.30 0.35 0.20 0.15 Variance Rate of

Consider the following information: Probability State of of State of Economy Boom Good Poor Bust Expected return Economy 0.30 0.35 0.20 0.15 Variance Rate of Return if State Occurs Stock A 0.20 0.17 -0.01 -0.09 a. Your portfolio is invested 30 percent each in Stocks A and C and 40 percent in Stock B. What is the expected return of the portfolio? Note: Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places. Stock B 0.36 0.24 -0.09 -0.20 % Stock C 0.27 0.09 -0.04 -0.10 b-1. What is the variance of this portfolio? Note: Do not round intermediate calculations. Round your answer to 5 decimal places.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Methods And Finance

Authors: Emiliano Ippoliti, Ping Chen

1st Edition

3319498711, 978-3319498713