Answered step by step

Verified Expert Solution

Question

1 Approved Answer

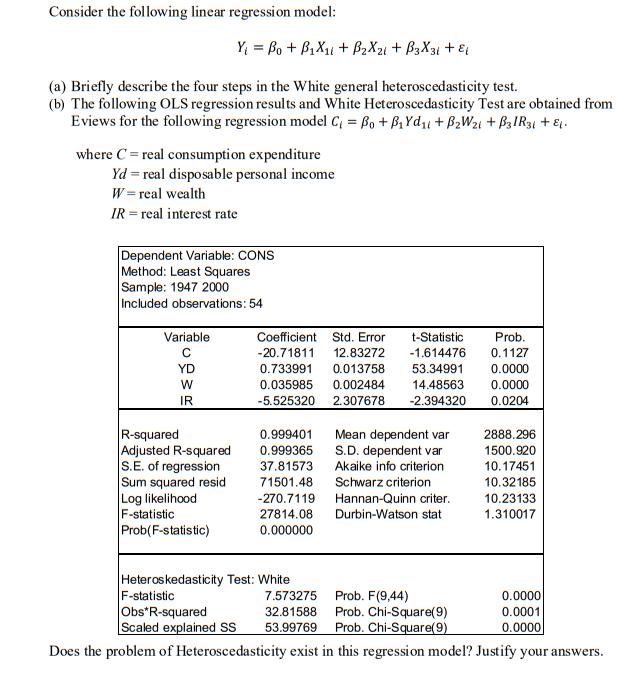

Consider the following linear regression model: (a) Briefly describe the four steps in the White general heteroscedasticity test. (b) The following OLS regression results

Consider the following linear regression model: (a) Briefly describe the four steps in the White general heteroscedasticity test. (b) The following OLS regression results and White Heteroscedasticity Test are obtained from Eviews for the following regression model C = Bo + BYd + BW1 + B3IR31 + 1. where C= real consumption expenditure Yd = real disposable personal income W = real wealth IR = real interest rate Dependent Variable: CONS Method: Least Squares Sample: 1947 2000 Included observations: 54 Variable Y = Bo + BX1 + BX21 + B3X31 + E1 YD W IR R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) F-statistic Obs*R-squared t-Statistic Coefficient Std. Error -20.71811 12.83272 -1.614476 0.733991 0.013758 53.34991 0.035985 0.002484 14.48563 -5.525320 2.307678 -2.394320 0.999401 0.999365 37.81573 71501.48 -270.7119 27814.08 0.000000 Heteroskedasticity Test: White Mean dependent var S.D. dependent var Akaike info criterion Schwarz criterion Hannan-Quinn criter.. Durbin-Watson stat Prob. 0.1127 0.0000 0.0000 0.0204 2888.296 1500.920 10.17451 10.32185 10.23133 1.310017 7.573275 Prob. F(9,44) 32.81588 Prob. Chi-Square(9) Scaled explained SS 53.99769 Prob. Chi-Square(9) Does the problem of Heteroscedasticity exist in this regression model? Justify your answers. 0.0000 0.0001 0.0000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a The four steps in the white general heteroscedasticity test i Estimate the model using ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Basic Econometrics

Authors: Damodar N. Gujrati, Dawn C. Porter

5th edition

73375772, 73375779, 978-0073375779