Answered step by step

Verified Expert Solution

Question

1 Approved Answer

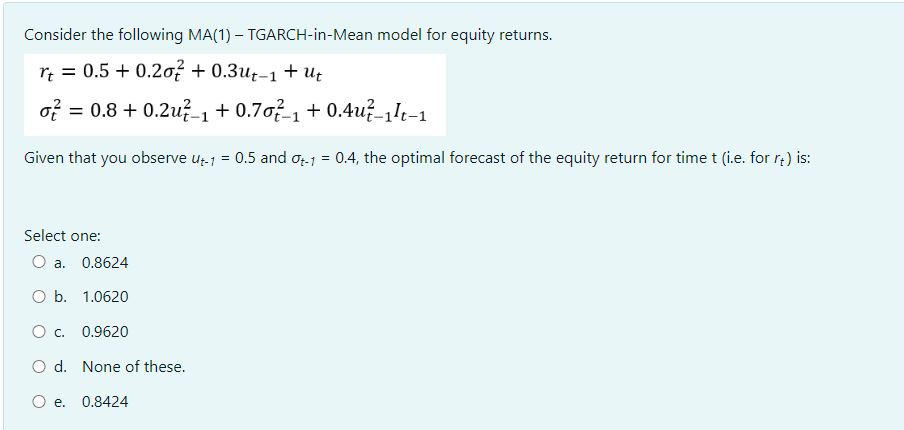

Consider the following MA(1) - TGARCH-in-Mean model for equity returns. rt=0.5+0.2t2+0.3ut1+utt2=0.8+0.2ut12+0.7t12+0.4ut12It1 Given that you observe ut1=0.5 and t1=0.4, the optimal forecast of the equity return

Consider the following MA(1) - TGARCH-in-Mean model for equity returns. rt=0.5+0.2t2+0.3ut1+utt2=0.8+0.2ut12+0.7t12+0.4ut12It1 Given that you observe ut1=0.5 and t1=0.4, the optimal forecast of the equity return for time t (i.e. for rt ) is: Select one: a. 0.8624 b. 1.0620 C. 0.9620 d. None of these. e. 0.8424 Consider the following MA(1) - TGARCH-in-Mean model for equity returns. rt=0.5+0.2t2+0.3ut1+utt2=0.8+0.2ut12+0.7t12+0.4ut12It1 Given that you observe ut1=0.5 and t1=0.4, the optimal forecast of the equity return for time t (i.e. for rt ) is: Select one: a. 0.8624 b. 1.0620 C. 0.9620 d. None of these. e. 0.8424

Consider the following MA(1) - TGARCH-in-Mean model for equity returns. rt=0.5+0.2t2+0.3ut1+utt2=0.8+0.2ut12+0.7t12+0.4ut12It1 Given that you observe ut1=0.5 and t1=0.4, the optimal forecast of the equity return for time t (i.e. for rt ) is: Select one: a. 0.8624 b. 1.0620 C. 0.9620 d. None of these. e. 0.8424 Consider the following MA(1) - TGARCH-in-Mean model for equity returns. rt=0.5+0.2t2+0.3ut1+utt2=0.8+0.2ut12+0.7t12+0.4ut12It1 Given that you observe ut1=0.5 and t1=0.4, the optimal forecast of the equity return for time t (i.e. for rt ) is: Select one: a. 0.8624 b. 1.0620 C. 0.9620 d. None of these. e. 0.8424 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: Harvey S. Rosen

5th Edition

025617329X, 978-0256173291