Answered step by step

Verified Expert Solution

Question

1 Approved Answer

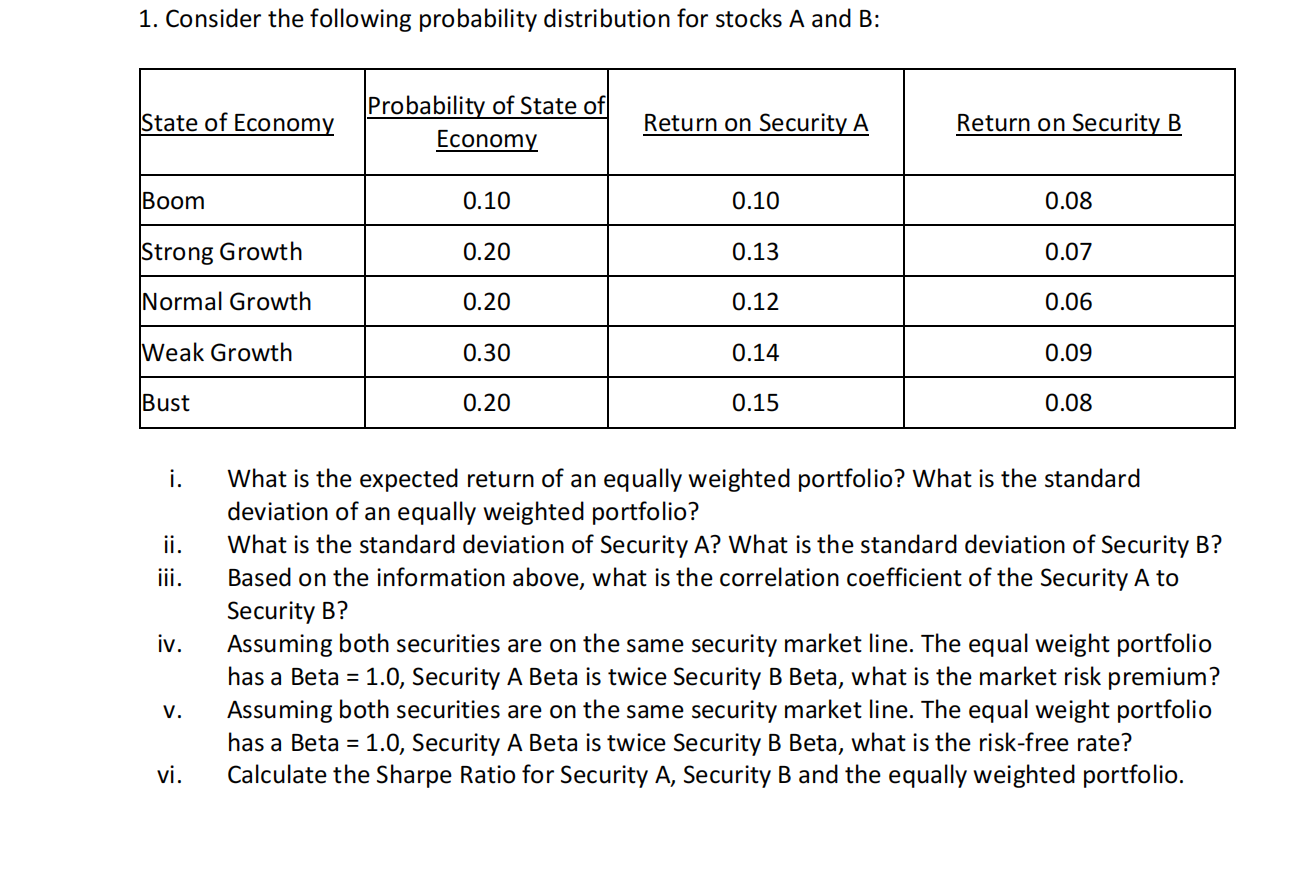

Consider the following probability distribution for stocks A and B : table [ [ State of Economy,Probability of State of , Return on Security

Consider the following probability distribution for stocks A and :

tableState of Economy,Probability of State ofReturn on Security AReturn on Security B Economy BoomStrong Growth,Normal Growth,Weak Growth,Bust

i What is the expected return of an equally weighted portfolio? What is the standard deviation of an equally weighted portfolio?

ii What is the standard deviation of Security A What is the standard deviation of Security B

iii. Based on the information above, what is the correlation coefficient of the Security A to Security B

iv Assuming both securities are on the same security market line. The equal weight portfolio has a Beta Security A Beta is twice Security B Beta, what is the market risk premium?

v Assuming both securities are on the same security market line. The equal weight portfolio has a Beta Security A Beta is twice Security B Beta, what is the riskfree rate?

vi Calculate the Sharpe Ratio for Security A Security B and the equally weighted portfolio.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investor Decision Making And The Role Of The Financial Advisor A Behavioural Finance Approach

Authors: Caterina Cruciani

1st Edition

3319682334,3319682342