Question

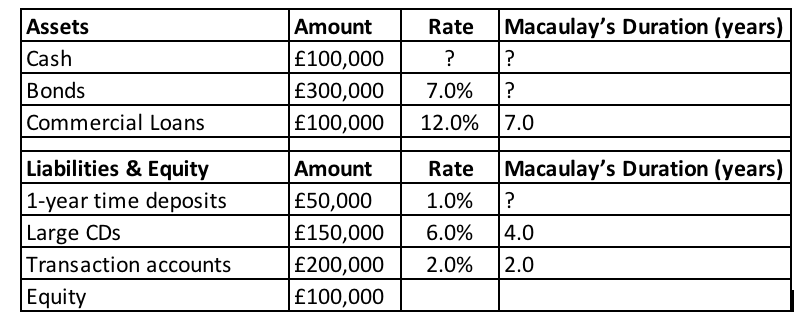

Consider the following summarised balance-sheet and associated average interest rates of a bank. The bank holds zero-coupon bonds that have a 4-year maturity with a

Consider the following summarised balance-sheet and associated average interest rates of a bank. The bank holds zero-coupon bonds that have a 4-year maturity with a 7% discount rate. Amounts in the balance-sheet represent current market values.

Calculate the Macaulays Duration for the banks bonds.

Amount Rate ? Macaulay's Duration (years) ? Assets Cash Bonds Commercial Loans 100,000 300,000 100,000 7.0% ? 12.0% 7.0 Macaulay's Duration (years) ? Liabilities & Equity 1-year time deposits Large CDs Transaction accounts Equity Amount 50,000 150,000 200,000 100,000 Rate 1.0% 6.0% 2.0% 4.0 2.0Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The ACT Guide To Ethical Conflicts In Finance

Authors: Andreas Prindl, Bimal Prodhan

1st Edition

1855732564, 978-1855732568