Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Consider the following: The Namibian risk-free rate is 3.75 percent, the US risk-free rate is 2.75 percent, and the spot exchange rate between the United

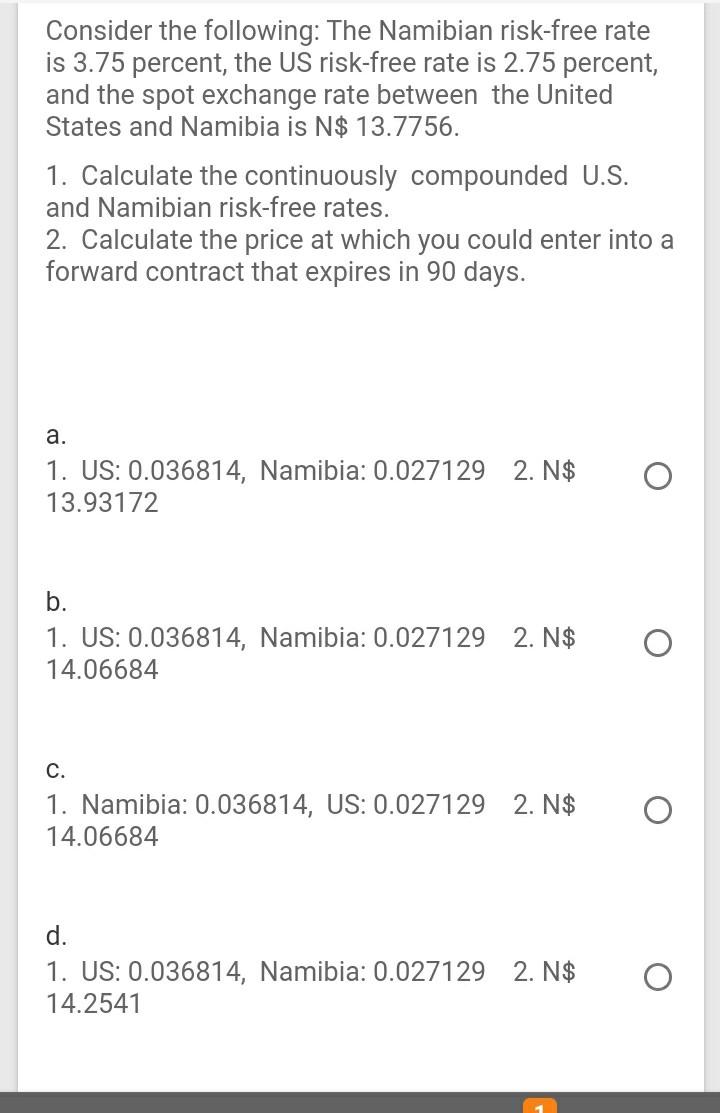

Consider the following: The Namibian risk-free rate is 3.75 percent, the US risk-free rate is 2.75 percent, and the spot exchange rate between the United States and Namibia is N$ 13.7756. 1. Calculate the continuously compounded U.S. and Namibian risk-free rates. 2. Calculate the price at which you could enter into a forward contract that expires in 90 days. a. 1. US: 0.036814, Namibia: 0.027129 13.93172 2. N$ b. 1. US: 0.036814, Namibia: 0.027129 2. N$ 14.06684 C. 1. Namibia: 0.036814, US: 0.027129 2. N$ 14.06684 d. 1. US: 0.036814, Namibia: 0.027129 2. N$ 14.2541 O

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started