Answered step by step

Verified Expert Solution

Question

1 Approved Answer

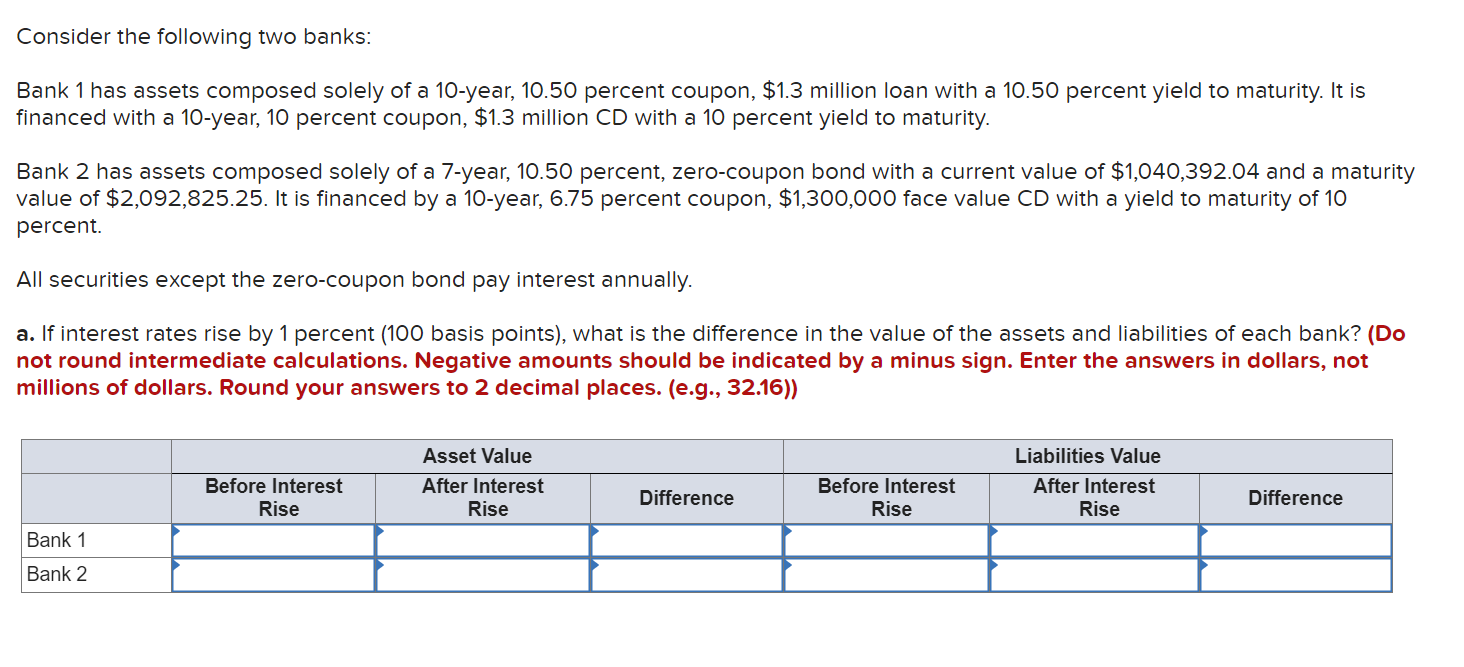

Consider the following two banks: Bank 1 has assets composed solely of a 1 0 - year, 1 0 . 5 0 percent coupon, $

Consider the following two banks:

Bank has assets composed solely of a year, percent coupon, $ million loan with a percent yield to maturity. It is financed with a year, percent coupon, $ million with a percent yield to maturity.

Bank has assets composed solely of a year, percent, zerocoupon bond with a current value of $ and a maturity value of $ It is financed by a year, percent coupon, $ face value with a yield to maturity of percent.

All securities except the zerocoupon bond pay interest annually.

a If interest rates rise by percent basis points what is the difference in the value of the assets and liabilities of each bank? Do not round intermediate calculations. Negative amounts should be indicated by a minus sign. Enter the answers in dollars, not millions of dollars. Round your answers to decimal places. eg

tableAsset Value,,Liabilities ValuetableBefore InterestRisetableAfter InterestRiseDifference,tableBefore InterestRisetableAfter InterestRiseBank Bank

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of Private Equity

Authors: Douglas Cumming

1st Edition

0195391586, 978-0195391589