Answered step by step

Verified Expert Solution

Question

1 Approved Answer

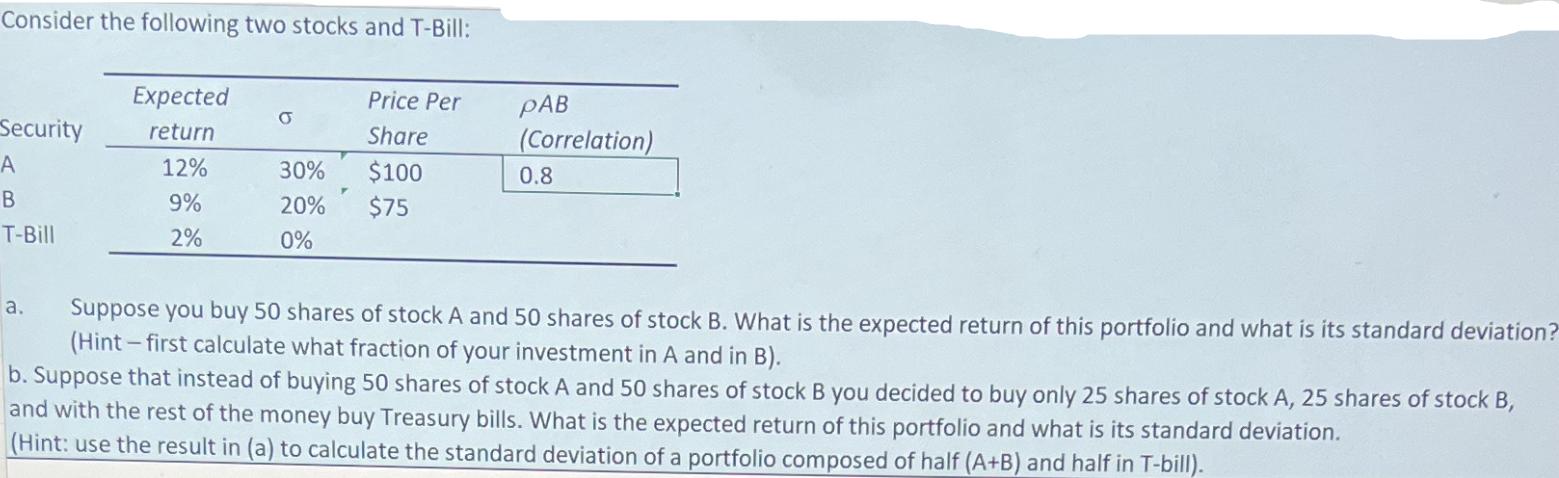

Consider the following two stocks and T-Bill: Security A B T-Bill a. Expected return 12% 9% 2% O Price Per Share 30% $100 20%

Consider the following two stocks and T-Bill: Security A B T-Bill a. Expected return 12% 9% 2% O Price Per Share 30% $100 20% $75 0% PAB (Correlation) 0.8 Suppose you buy 50 shares of stock A and 50 shares of stock B. What is the expected return of this portfolio and what is its standard deviation? (Hint - first calculate what fraction of your investment in A and in B). b. Suppose that instead of buying 50 shares of stock A and 50 shares of stock B you decided to buy only 25 shares of stock A, 25 shares of stock B, and with the rest of the money buy Treasury bills. What is the expected return of this portfolio and what is its standard deviation. (Hint: use the result in (a) to calculate the standard deviation of a portfolio composed of half (A+B) and half in T-bill).

Step by Step Solution

★★★★★

3.44 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

Lets calculate the expected return and standard deviation for each scenario a Portfolio with 50 shares of stock A and 50 shares of stock B First lets ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516