Answered step by step

Verified Expert Solution

Question

1 Approved Answer

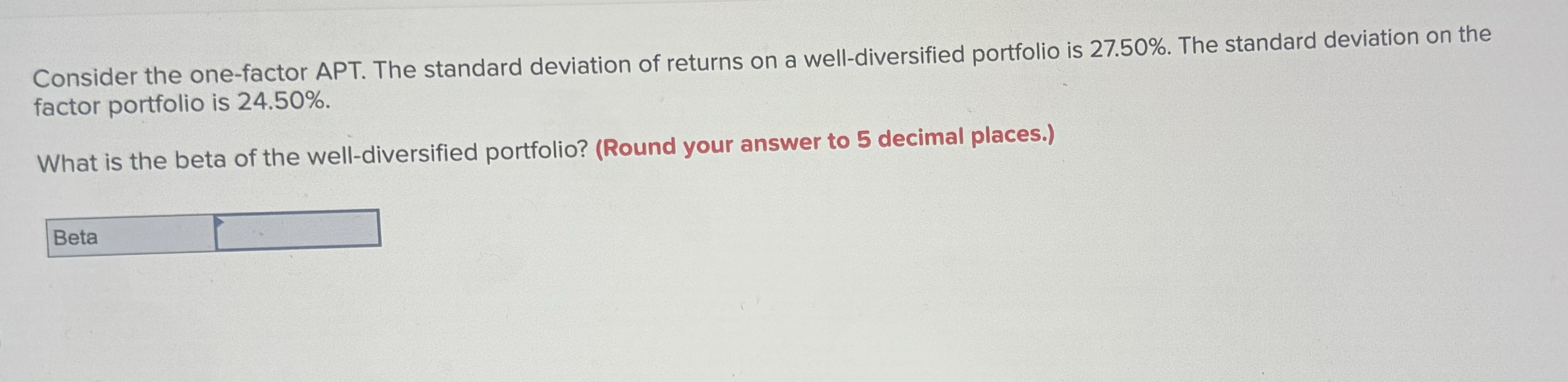

Consider the one - factor APT. The standard deviation of returns on a well - diversified portfolio is 2 7 . 5 0 % .

Consider the onefactor APT. The standard deviation of returns on a welldiversified portfolio is The standard deviation on the factor portfolio is

What is the beta of the welldiversified portfolio? Round your answer to decimal places.

Beta

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

University Finances Accounting And Budgeting Principles For Higher Education

Authors: Dean O. Smith

1st Edition

1421427257, 978-1421427256