Question

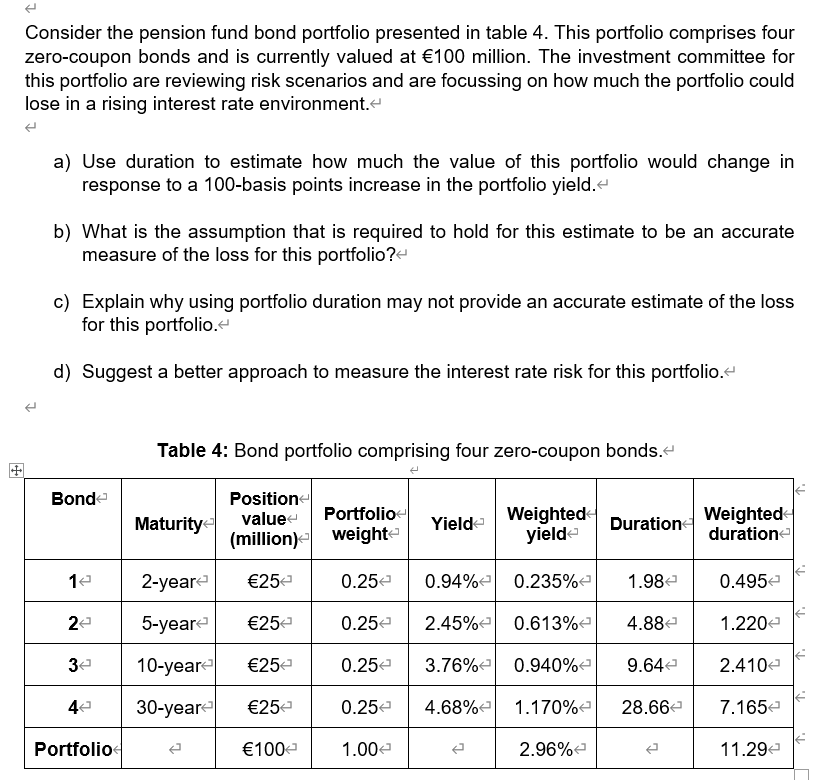

Consider the pension fund bond portfolio presented in table 4. This portfolio comprises four zero-coupon bonds and is currently valued at 100 million. The investment

Consider the pension fund bond portfolio presented in table 4. This portfolio comprises four zero-coupon bonds and is currently valued at 100 million. The investment committee for this portfolio are reviewing risk scenarios and are focussing on how much the portfolio could lose in a rising interest rate environment. a) Use duration to estimate how much the value of this portfolio would change in response to a 100-basis points increase in the portfolio yield. b) What is the assumption that is required to hold for this estimate to be an accurate measure of the loss for this portfolio? c) Explain why using portfolio duration may not provide an accurate estimate of the loss for this portfolio. d) Suggest a better approach to measure the interest rate risk for this portfolio.

table 4. This portfolio comprises four zero-coupon bonds and is currently valued at 100 million. The investment committee for this portfolio are reviewing risk scenarios and are focussing on how much the portfolio could lose in a rising interest rate environment. a) Use duration to estimate how much the value of this portfolio would change in response to a 100-basis points increase in the portfolio yield. b) What is the assumption that is required to hold for this estimate to be an accurate measure of the loss for this portfolio? c) Explain why using portfolio duration may not provide an accurate estimate of the loss for this portfolio. d) Suggest a better approach to measure the interest rate risk for this portfolio.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forex Definitive Beginner S Guide

Authors: Brian Stclair

1st Edition

1537664670, 978-1537664675