Answered step by step

Verified Expert Solution

Question

1 Approved Answer

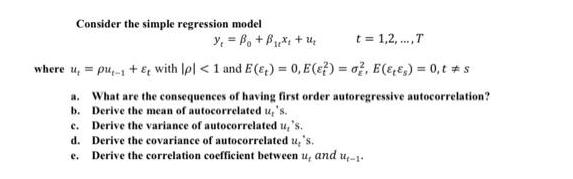

Consider the simple regression model Y =B + Bx +4 t = 1,2, ...,T where u, pu, + & with lpl < 1 and

Consider the simple regression model Y =B + Bx +4 t = 1,2, ...,T where u, pu, + & with lpl < 1 and E(e) = 0, E(?) = o?, E(EE) = 0,t #s a. What are the consequences of having first order autoregressive autocorrelation? b. Derive the mean of autocorrelated u,'s. c. Derive the variance of autocorrelated u,'s. d. Derive the covariance of autocorrelated u, 's. e. Derive the correlation coefficient between u, and 1-1.

Step by Step Solution

★★★★★

3.42 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

The consequences of having firstorder autoregressive AR1 autocorrelation in the regression model are as follows a The model assumes that the error ter...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introductory Econometrics A Modern Approach

Authors: Jeffrey M. Wooldridge

4th edition

978-0324581621, 324581629, 324660545, 978-0324660548