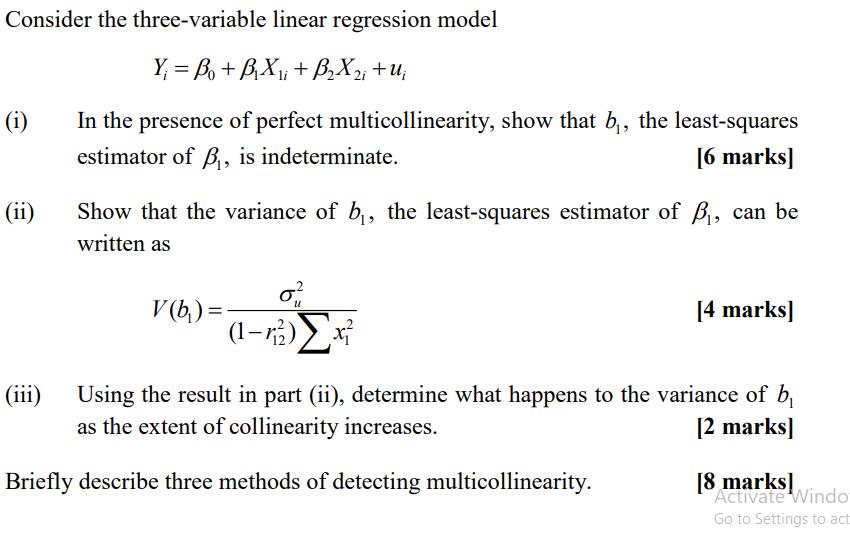

Question: Consider the three-variable linear regression model Y = Bo +BX + BX, tui (i) (ii) (iii) In the presence of perfect multicollinearity, show that

Consider the three-variable linear regression model Y = Bo +BX + BX, tui (i) (ii) (iii) In the presence of perfect multicollinearity, show that b, the least-squares estimator of P, is indeterminate. [6 marks] Show that the variance of b, the least-squares estimator of , can be written as V (b) = u (1-13) [4 marks] Using the result in part (ii), determine what happens to the variance of b as the extent of collinearity increases. [2 marks] Briefly describe three methods of detecting multicollinearity. [8 marks] Activate Windo Go to Settings to act

Step by Step Solution

There are 3 Steps involved in it

Answer Let solve the question step by step STEP 1 In the presence of perfect multicollinearity the model is as follows Y B2 B1X1 B2X2 u Perfect multic... View full answer

Get step-by-step solutions from verified subject matter experts