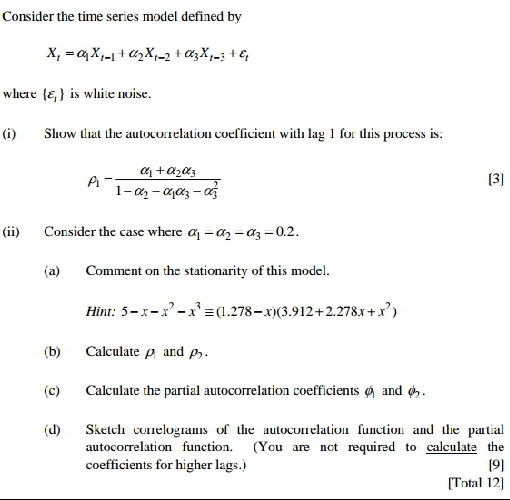

Consider the time series model defined by X =x-ax-2 +3X-3 +&+ where {E} is white noise. (i) Show that the autocorrelation coefficient with lag

Consider the time series model defined by X =x-ax-2 +3X-3 +&+ where {E} is white noise. (i) Show that the autocorrelation coefficient with lag 1 for this process is: Pi - (ii) Consider the case where a-02-03 -0.2. (a) Comment on the stationarity of this model. Hint: 5-x-x-x=(1.278-x)(3.912+2.278x+x) (b) Calculate p and p. [3] (c) Calculate the partial autocorrelation coefficients and . T (d) Sketch comelograms of the autocorrelation function and the partial autocorrelation function. (You are not required to calculate the coefficients for higher lags.) [9] [Total 12]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Barry Monk

2nd edition

1259345297, 978-0077836351, 77836359, 978-1259295911, 1259295915, 978-1259292484, 1259292487, 978-1259345296