Question

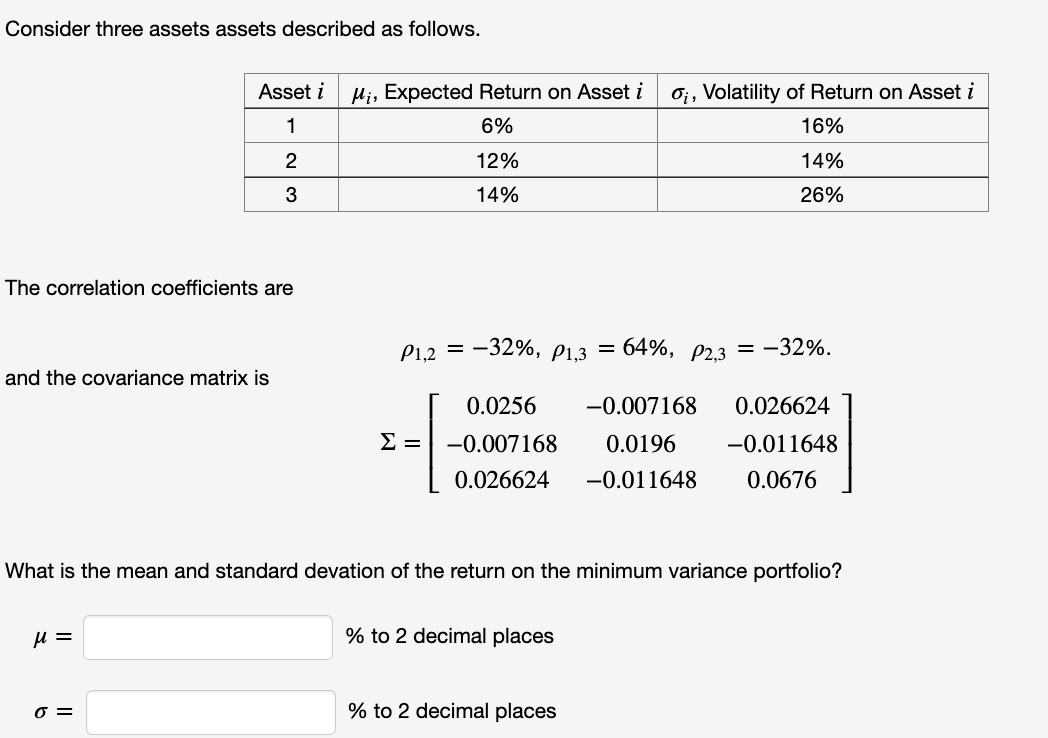

Consider three assets assets described as follows. Asset ii ii, Expected Return on Asset ii ii, Volatility of Return on Asset ii 1 6% 16%

Consider three assets assets described as follows.

| Asset ii | ii, Expected Return on Asset ii | ii, Volatility of Return on Asset ii |

| 1 | 6% | 16% |

| 2 | 12% | 14% |

| 3 | 14% | 26% |

The correlation coefficients are

1,2=321,2=32%, 1,3=641,3=64%, 2,3=322,3=32%.

and the covariance matrix is

=0.02560.0071680.0266240.0071680.01960.0116480.0266240.0116480.0676=[0.02560.0071680.0266240.0071680.01960.0116480.0266240.0116480.0676]

What is the mean and standard devation of the return on the minimum variance portfolio? == % to 2 decimal places == % to 2 decimal places

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin Revolution Discover The Principles Of Bitcoin Mining

Authors: Lin Saurel

1st Edition

979-8353001966