Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Consider two coupon bonds. The first coupon bond has a coupon of C(1) = 2, M = 100, and n = 2. The second

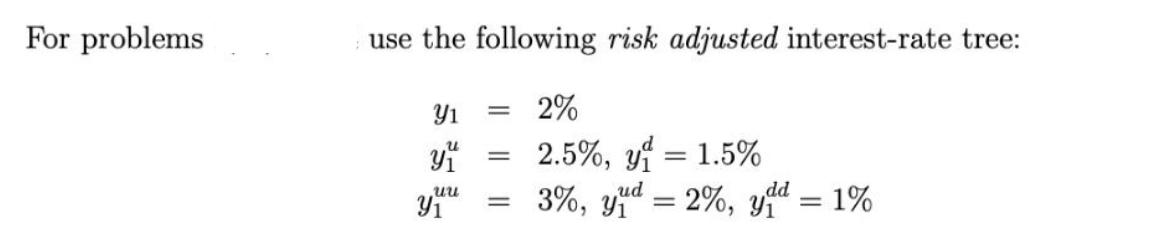

Consider two coupon bonds. The first coupon bond has a coupon of C(1) = 2, M = 100, and n = 2. The second bond has a coupon of C(2) = 2, M = 100, and n = 3. Also, consider a futures contract where the short side has the option to deliver either the first or the second bond at time 1 (assume the conversion factor for both bonds to be y = = 1). Calculate the futures price. For problems use the following risk adjusted interest-rate tree: 2% 2.5%, y = 1.5% 3%, yud - 2%, ydd = 1% Y y uu 31 - = =

Step by Step Solution

★★★★★

3.41 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

Solution To calculate the futures price we need to calculate the present value of the future cash fl...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets and Institutions

Authors: Anthony Saunders, Marcia Cornett

6th edition

9780077641849, 77861663, 77641841, 978-0077861667