Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Consider two risky assets: a stock fund and a bond fund with the following probability distributions. Scenario Please show your work so I can understand

Consider two risky assets: a stock fund and a bond fund with the following probability distributions. Scenario

Please show your work so I can understand how to complete this. Thank you.

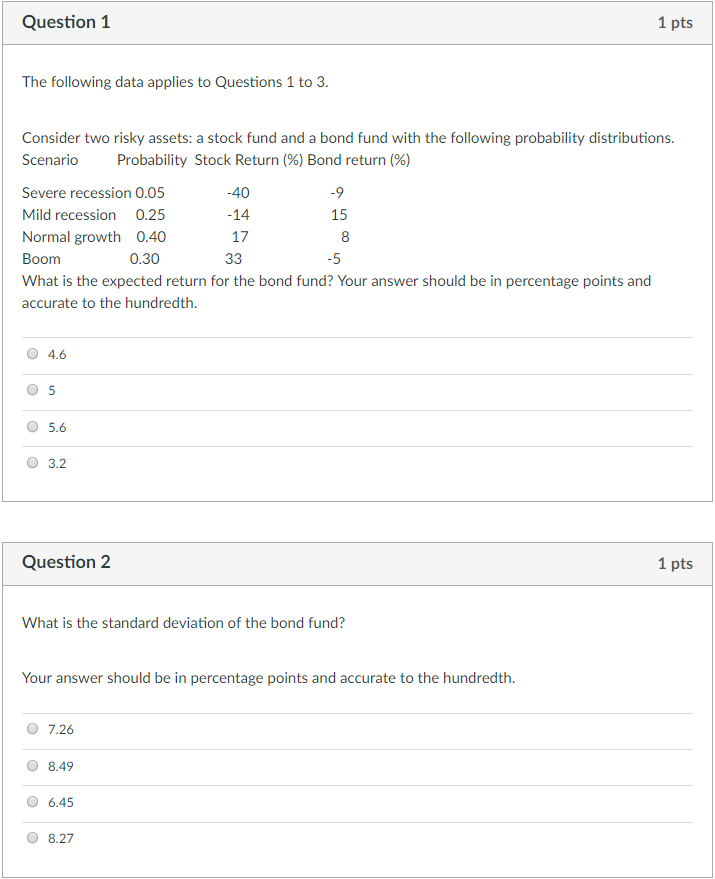

Question 1 1 pts The following data applies to Questions 1 to 3 Consider two risky assets: a stock fund and a bond fund with the following probability distributions. Scenario Probability Stock Return (%) Bond return (%) Severe recession 0.05 Mild recession 0.25 Normal growth 0.40 Boom What is the expected return for the bond fund? Your answer should be in percentage points and accurate to the hundredth -40 -14 17 15 0.30 -5 O 4.6 O 5 O 5.6 O 3.2 Question 2 1 pts What is the standard deviation of the bond fund? Your answer should be in percentage points and accurate to the hundredth O 7.26 O 8.49 O 6.45 O 8.27Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied Valuation A Pragmatic Approach

Authors: Clifford S. Ang

1st Edition

3110771748,3110771837