Answered step by step

Verified Expert Solution

Question

1 Approved Answer

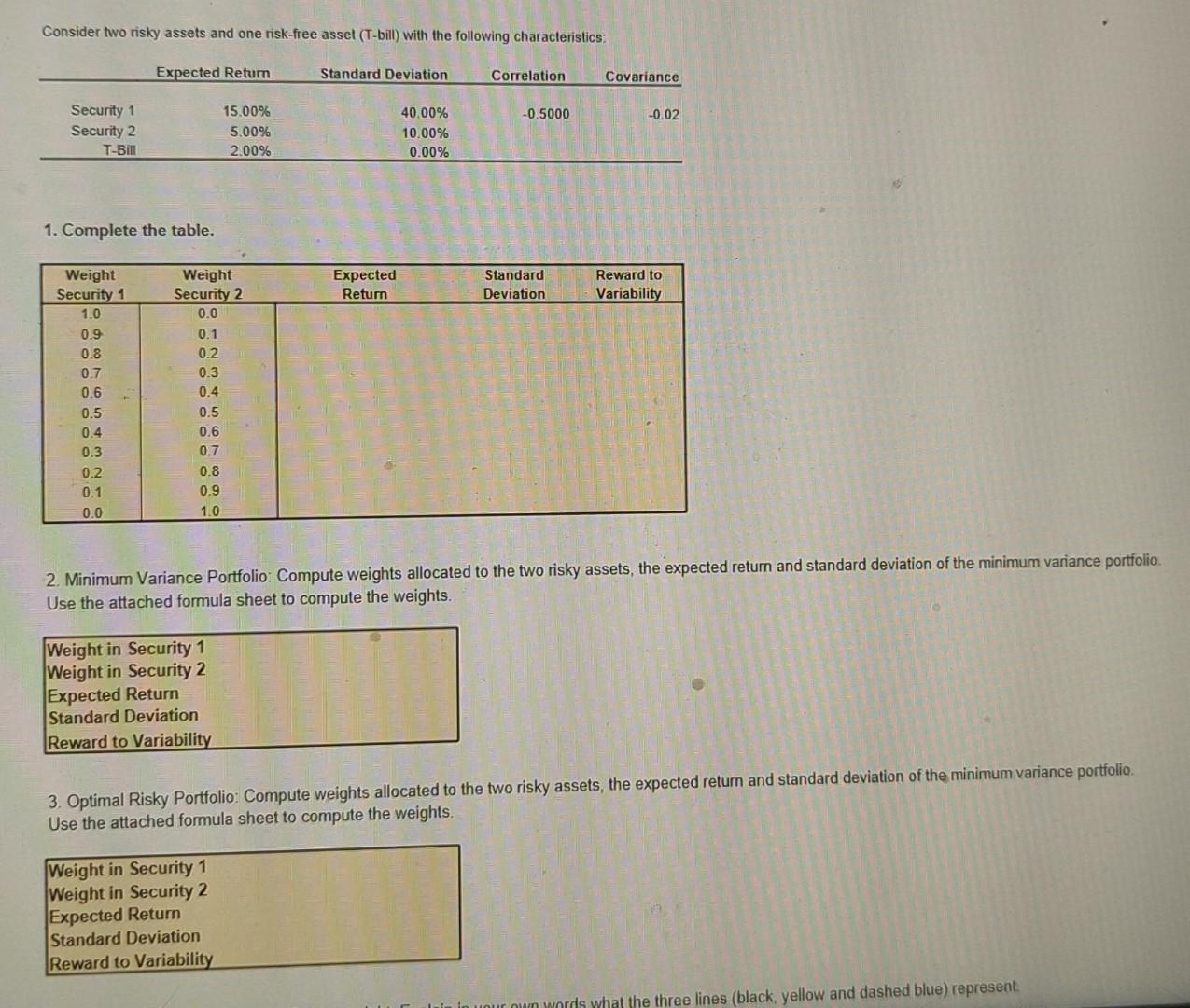

Consider two risky assets and one risk-free asset (T-bill) with the following characteristics: 1. Complete the table. 2. Minimum Variance Portfolio: Compute weights allocated to

Consider two risky assets and one risk-free asset (T-bill) with the following characteristics: 1. Complete the table. 2. Minimum Variance Portfolio: Compute weights allocated to the two risky assets, the expected return and standard deviation of the minimum variance portfolio. Use the attached formula sheet to compute the weights. 3. Optimal Risky Portfolio: Compute weights allocated to the two risky assets, the expected return and standard deviation of the minimum variance portfolio. Use the attached formula sheet to compute the weights. \begin{tabular}{|l|} \hline Weight in Security 1 \\ Weight in Security 2 \\ Expected Return \\ Standard Deviation \\ Reward to Variability \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Budget Building Book For Nonprofits

Authors: Murray Dropkin, Jim Halpin, Bill La Touche

2nd Edition

0787996033, 978-0787996031