Answered step by step

Verified Expert Solution

Question

1 Approved Answer

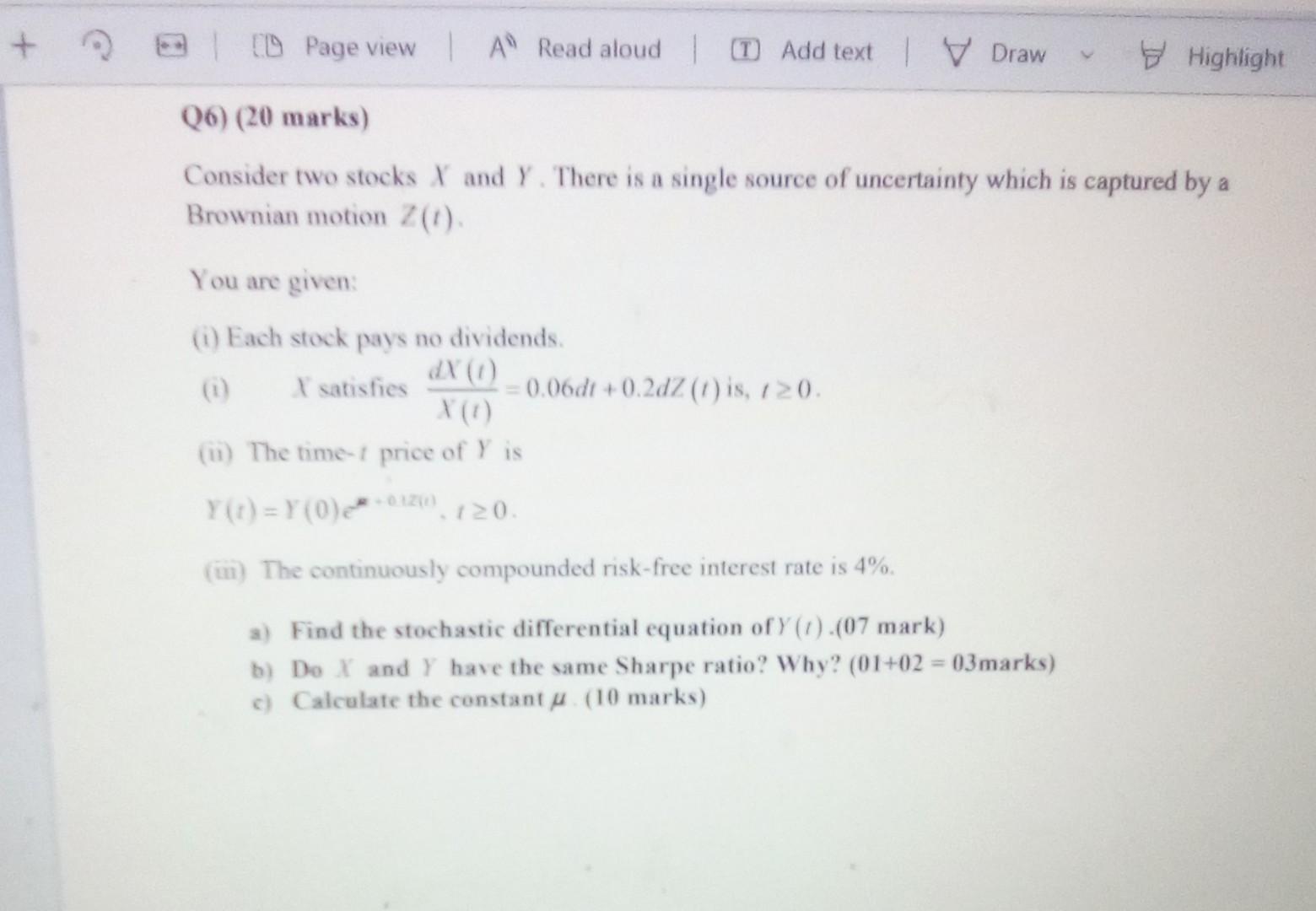

Consider two stocks X and Y. There is a single source of uncertainty which is captured by a Brownian motion Z(t). You are given: (i)

Consider two stocks X and Y. There is a single source of uncertainty which is captured by a Brownian motion Z(t). You are given: (i) Each stock pays no dividends. (i) X satisfies X(t)dX(t)=0.06dt+0.2dZ(t) is, t0. (ii) The time-t price of Y is Y(t)=Y(0)em+012(0),t0. (iii) The continuously compounded risk-free interest rate is 4%. a) Find the stochastic differential equation of Y(t).(07 mark) b) Do X and Y have the same Sharpe ratio? Why? (01+02=03 marks ) c) Calculate the constant . (10 marks) Consider two stocks X and Y. There is a single source of uncertainty which is captured by a Brownian motion Z(t). You are given: (i) Each stock pays no dividends. (i) X satisfies X(t)dX(t)=0.06dt+0.2dZ(t) is, t0. (ii) The time-t price of Y is Y(t)=Y(0)em+012(0),t0. (iii) The continuously compounded risk-free interest rate is 4%. a) Find the stochastic differential equation of Y(t).(07 mark) b) Do X and Y have the same Sharpe ratio? Why? (01+02=03 marks ) c) Calculate the constant . (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ISE Fundamental Managerial Accounting Concepts

Authors: Thomas Edmonds, Christopher Edmonds, Mark Edmonds, Philip Olds

9th Edition

1260565483, 9781260565485