Answered step by step

Verified Expert Solution

Question

1 Approved Answer

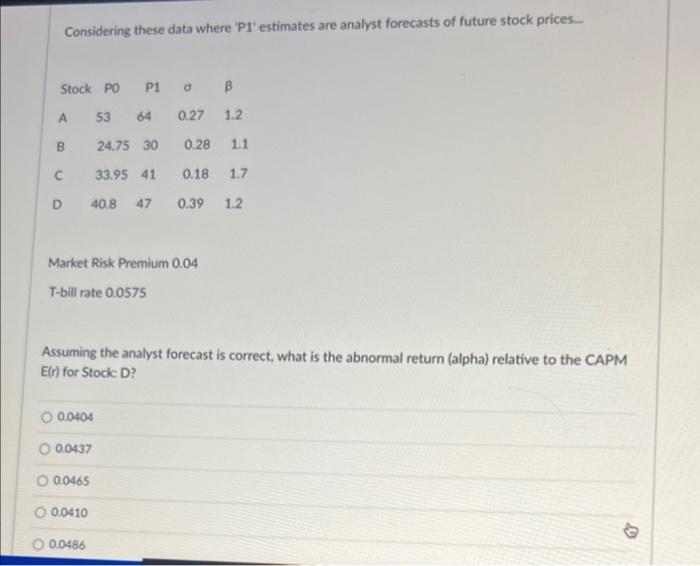

Considering these data where 'P1' estimates are analyst forecasts of future stock prices..... B 53 64 0.27 1.2 24.75 30 0.28 1.1 C 33.95 41

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Passive Income Stacking Handbook How To Reach Financial Freedom Faster Regardless Of Your Age Or Situation

Authors: Mark Walters

1st Edition

0578530171, 978-0578530178