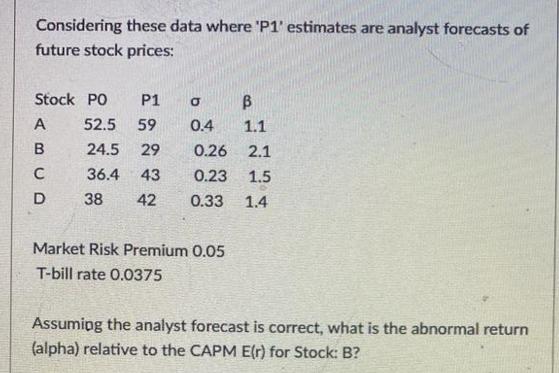

Considering these data where 'P1' estimates are analyst forecasts of future stock prices: Stock PO P1 A B C D B 52.5 59 0.4

Considering these data where 'P1' estimates are analyst forecasts of future stock prices: Stock PO P1 A B C D B 52.5 59 0.4 1.1 24.5 29 0.26 2.1 36.4 43 0.23 1.5 38 42 0.33 1.4 Market Risk Premium 0.05 T-bill rate 0.0375 Assuming the analyst forecast is correct, what is the abnormal return (alpha) relative to the CAPM E(r) for Stock: B?

Step by Step Solution

3.56 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

Actual return P1POPO 65525 1238 CAPM return Risk...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516