Answered step by step

Verified Expert Solution

Question

1 Approved Answer

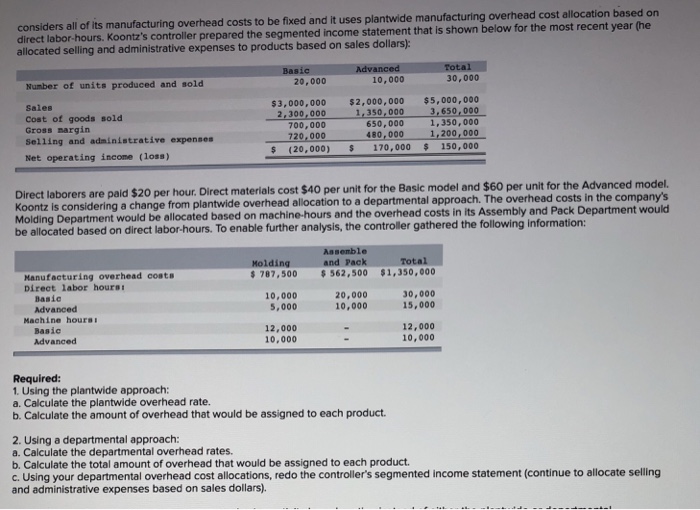

considers all of its manufacturing overhead costs to be fixed and it uses plantwide manufacturing overhead cost allocation based on abor-hours. Koontz's controller prepared the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Process Safety Management Risk Management Planning Auditing Handbook A Checklist Approach

Authors: David Einolf, Luverna Menghini

1st Edition

086587686X, 978-0865876866