Answered step by step

Verified Expert Solution

Question

1 Approved Answer

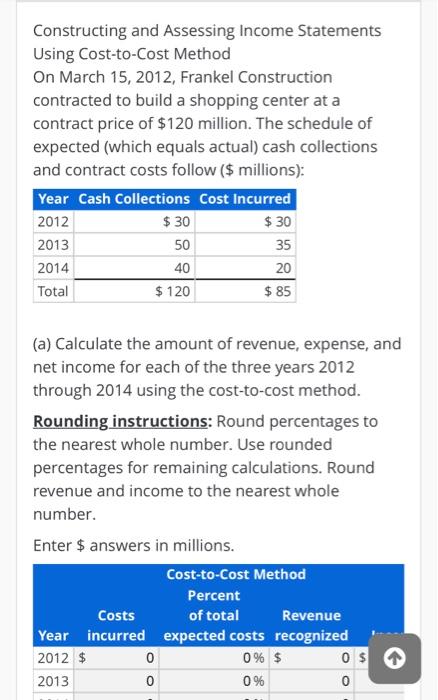

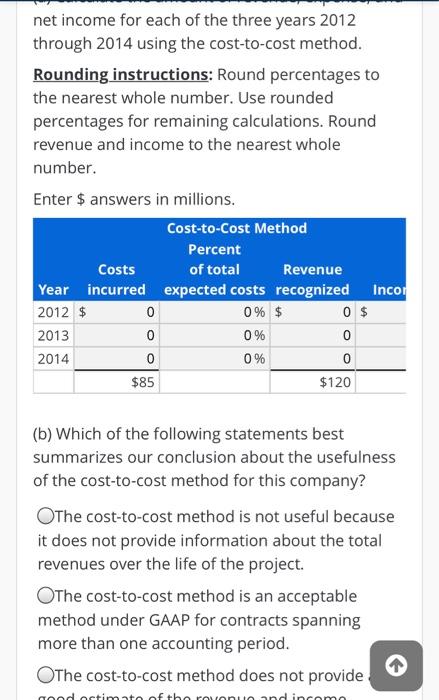

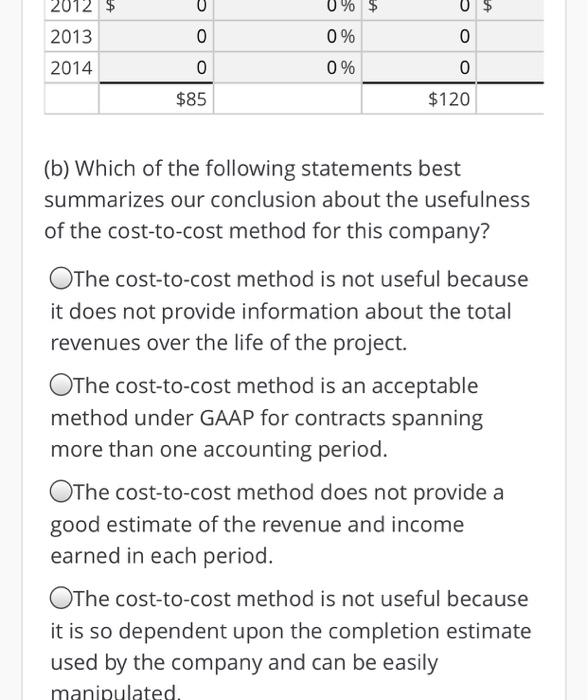

Constructing and Assessing Income Statements Using Cost-to-Cost Method On March 15, 2012, Frankel Construction contracted to build a shopping center at a contract price of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Auditing and Other Assurance Services

Authors: Ray Whittington, Kurt Pany

19th edition

978-0077804770, 78025613, 77804775, 978-0078025617