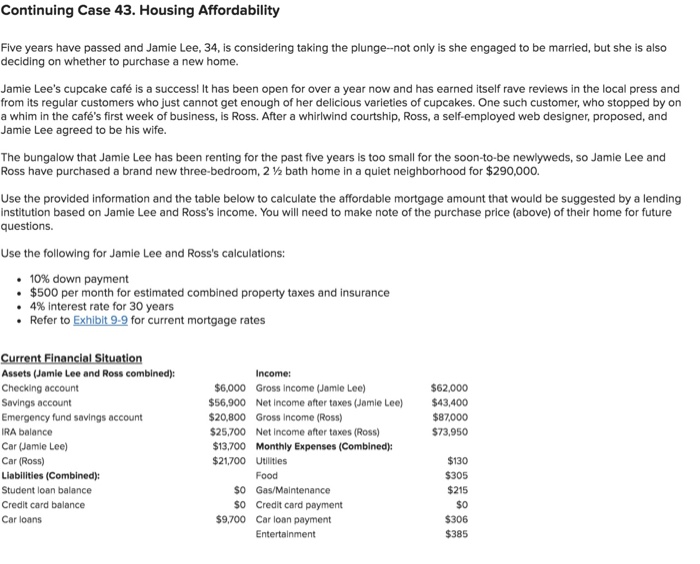

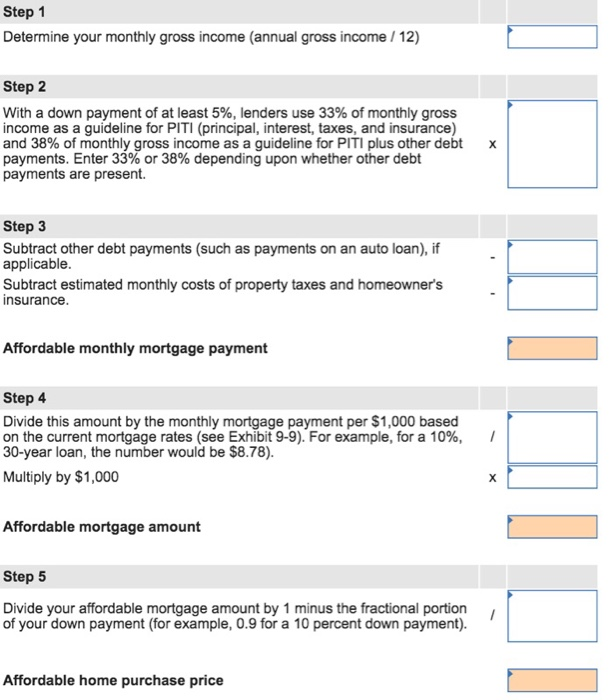

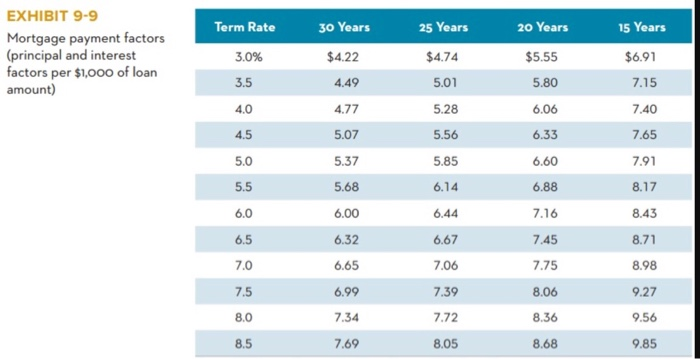

Continuing Case 43. Housing Affordability Five years have passed and Jamie Lee, 34, is considering taking the plunge-not only is she engaged to be married, but she is also deciding on whether to purchase a new home. Jamie Lee's cupcake caf is a success! It has been open for over a year now and has earned itself rave reviews in the local press and from its regular customers who just cannot get enough of her delicious varieties of cupcakes. One such customer, who stopped by on a whim in the caf's first week of business, is Ross. After a whirlwind courtship, Ross, a self-employed web designer, proposed, and Jamie Lee agreed to be his wife. The bungalow that Jamie Lee has been renting for the past five years is too small for the soon-to-be newlyweds, so Jamie Lee and Ross have purchased a brand new three-bedroom, 2 bath home in a quiet neighborhood for $290,000. Use the provided information and the table below to calculate the affordable mortgage amount that would be suggested by a lending institution based on Jamie Lee and Ross's income. You will need to make note of the purchase price (above) of their home for future questions. Use the following for Jamie Lee and Ross's calculations: 10% down payment $500 per month for estimated combined property taxes and insurance 4% interest rate for 30 years Refer to Exhibit 9-9 for current mortgage rates Current Financial Situation Assets (Jamie Lee and Ross combined): Checking account Income: $6,000 Gross Income (Jamie Lee) $62,000 $56,900 Net income after taxes (Jamie Lee) $43,400 Savings account $20,800 Gross income (Ross) Emergency fund savings account $87,000 $73,950 IRA balance $25,700 Net income after taxes (Ross) Car (Jamie Lee) $13,700 Monthly Expenses (Combined): $21,700 Utilities Car (Ross) $130 $305 Liabilities (Combined): Food so Gas/Maintenance so Credit card payment Student loan balance $215 Credit card balance $0 Car loans $9,700 $306 Car loan payment Entertainment $385 Step 1 Determine your monthly gross income (annual gross income / 12) Step 2 With a down payment of at least 5%, lenders use 33% of monthly gross income as a guideline for PITI (principal, interest, taxes, and insurance) and 38% of monthly gross income as a guideline for PITI plus other debt payments. Enter 33% or 38% depending upon whether other debt payments are present. Step 3 Subtract other debt payments (such as payments on an auto loan), if applicable. Subtract estimated monthly costs of property taxes and homeowner's insurance. Affordable monthly mortgage payment Step 4 Divide this amount by the monthly mortgage payment per $1,000 based on the current mortgage rates (see Exhibit 9-9). For example, for a 10%, 30-year loan, the number would be $8.78). Multiply by $1,000 Affordable mortgage amount Step 5 Divide your affordable mortgage amount by 1 minus the fractional portion of your down payment (for example, 0.9 for a 10 percent down payment). Affordable home purchase price EXHIBIT 9-9 Term Rate 30 Years 25 Years 20 Years 15 Years Mortgage payment factors (principal and interest factors per $1,000 of loan amount) $6.91 $4.22 $4.74 $5.55 3.0% 5.80 3.5 4.49 5.01 7.15 7.40 6.06 4.0 4.77 5.28 5.07 6.33 4.5 5.56 7.65 5.85 7.91 5.0 5.37 6.60 5.5 5.68 6.14 6.88 8.17 7.16 6.0 6.00 6.44 8.43 6.5 6.32 6.67 7.45 8.71 7.0 7.06 7.75 8.98 6.65 7.5 6.99 7.39 8.06 9.27 7.34 7.72 8.36 8.0 9.56 9.85 8.5 7.69 8.05 8.68 Continuing Case 43. Housing Affordability Five years have passed and Jamie Lee, 34, is considering taking the plunge-not only is she engaged to be married, but she is also deciding on whether to purchase a new home. Jamie Lee's cupcake caf is a success! It has been open for over a year now and has earned itself rave reviews in the local press and from its regular customers who just cannot get enough of her delicious varieties of cupcakes. One such customer, who stopped by on a whim in the caf's first week of business, is Ross. After a whirlwind courtship, Ross, a self-employed web designer, proposed, and Jamie Lee agreed to be his wife. The bungalow that Jamie Lee has been renting for the past five years is too small for the soon-to-be newlyweds, so Jamie Lee and Ross have purchased a brand new three-bedroom, 2 bath home in a quiet neighborhood for $290,000. Use the provided information and the table below to calculate the affordable mortgage amount that would be suggested by a lending institution based on Jamie Lee and Ross's income. You will need to make note of the purchase price (above) of their home for future questions. Use the following for Jamie Lee and Ross's calculations: 10% down payment $500 per month for estimated combined property taxes and insurance 4% interest rate for 30 years Refer to Exhibit 9-9 for current mortgage rates Current Financial Situation Assets (Jamie Lee and Ross combined): Checking account Income: $6,000 Gross Income (Jamie Lee) $62,000 $56,900 Net income after taxes (Jamie Lee) $43,400 Savings account $20,800 Gross income (Ross) Emergency fund savings account $87,000 $73,950 IRA balance $25,700 Net income after taxes (Ross) Car (Jamie Lee) $13,700 Monthly Expenses (Combined): $21,700 Utilities Car (Ross) $130 $305 Liabilities (Combined): Food so Gas/Maintenance so Credit card payment Student loan balance $215 Credit card balance $0 Car loans $9,700 $306 Car loan payment Entertainment $385 Step 1 Determine your monthly gross income (annual gross income / 12) Step 2 With a down payment of at least 5%, lenders use 33% of monthly gross income as a guideline for PITI (principal, interest, taxes, and insurance) and 38% of monthly gross income as a guideline for PITI plus other debt payments. Enter 33% or 38% depending upon whether other debt payments are present. Step 3 Subtract other debt payments (such as payments on an auto loan), if applicable. Subtract estimated monthly costs of property taxes and homeowner's insurance. Affordable monthly mortgage payment Step 4 Divide this amount by the monthly mortgage payment per $1,000 based on the current mortgage rates (see Exhibit 9-9). For example, for a 10%, 30-year loan, the number would be $8.78). Multiply by $1,000 Affordable mortgage amount Step 5 Divide your affordable mortgage amount by 1 minus the fractional portion of your down payment (for example, 0.9 for a 10 percent down payment). Affordable home purchase price EXHIBIT 9-9 Term Rate 30 Years 25 Years 20 Years 15 Years Mortgage payment factors (principal and interest factors per $1,000 of loan amount) $6.91 $4.22 $4.74 $5.55 3.0% 5.80 3.5 4.49 5.01 7.15 7.40 6.06 4.0 4.77 5.28 5.07 6.33 4.5 5.56 7.65 5.85 7.91 5.0 5.37 6.60 5.5 5.68 6.14 6.88 8.17 7.16 6.0 6.00 6.44 8.43 6.5 6.32 6.67 7.45 8.71 7.0 7.06 7.75 8.98 6.65 7.5 6.99 7.39 8.06 9.27 7.34 7.72 8.36 8.0 9.56 9.85 8.5 7.69 8.05 8.68