Question

---- Convexity is used to correct the approximate percentage change in bond value, calculated using modified duration. Group of answer choices True False A bond

---- Convexity is used to correct the approximate percentage change in bond value, calculated using modified duration.

Group of answer choices

True

False

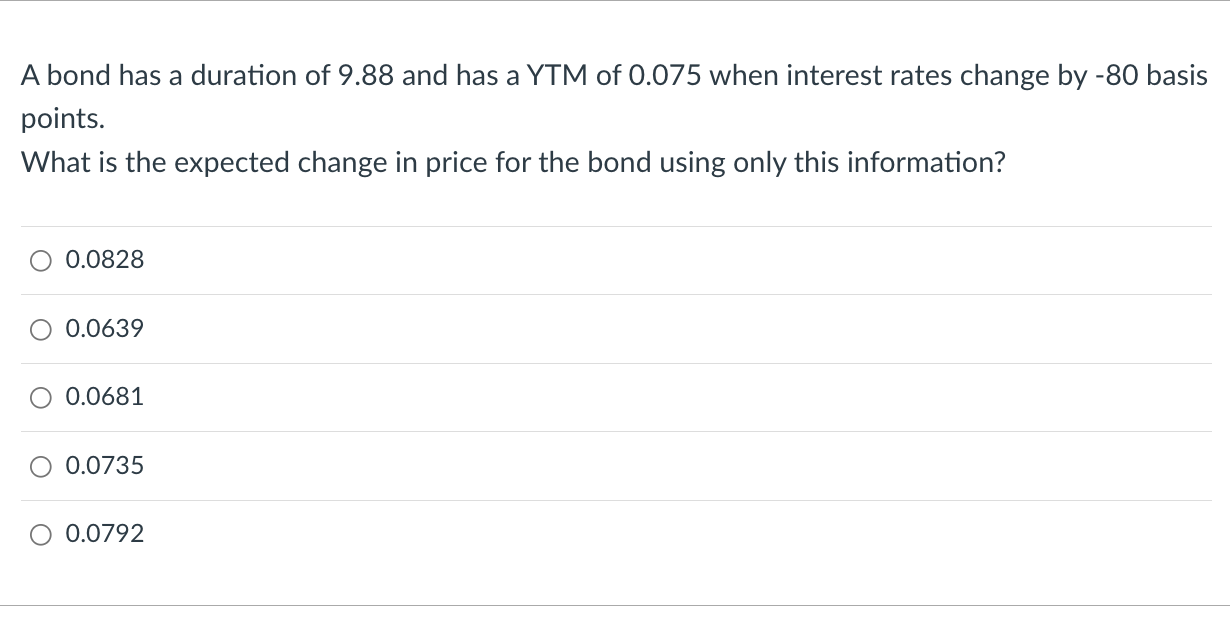

A bond has a duration of 9.88 and has a YTM of 0.075 when interest rates change by -80 basis points. What is the expected change in price for the bond using only this information? O 0.0828 0.0639 O 0.0681 O 0.0735 O 0.0792Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Future Of Financea The LSE Report

Authors: Chairman Adair Turner, Paul Woolley, Andrew Dr Haldane, Richard Layard, Andrew G. Haldane, Paul Wooley

1st Edition

085328458X, 978-0853284581