Answered step by step

Verified Expert Solution

Question

1 Approved Answer

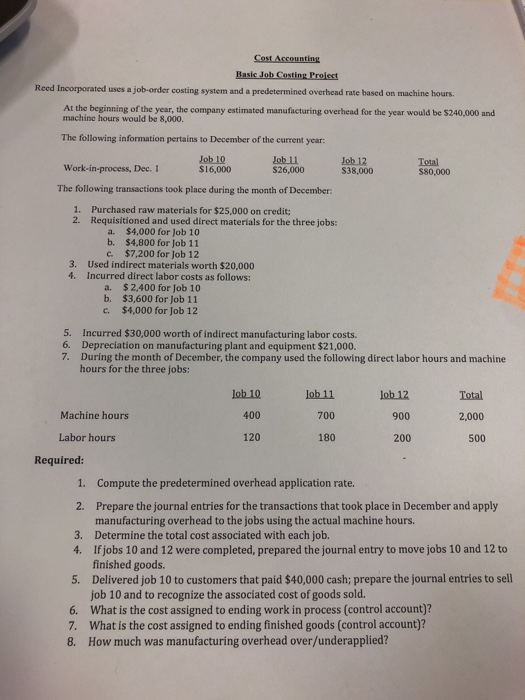

Cost Accounting Basic Job Costing Project Reed Incorporated uses a job-order costing system and a predetermined overhead rate based on machine hours. At the beginning

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Executive Roadmap To Fraud Prevention And Internal Control Creating A Culture Of Compliance

Authors: Joel T. Bartow, Martin T. Biegelman

2nd Edition

1118004582, 9781118004586