Answered step by step

Verified Expert Solution

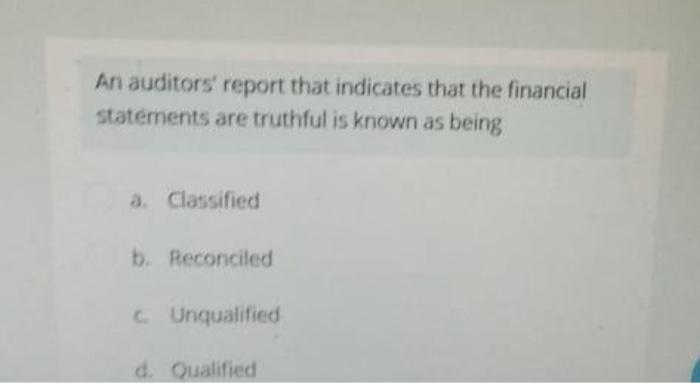

Question

1 Approved Answer

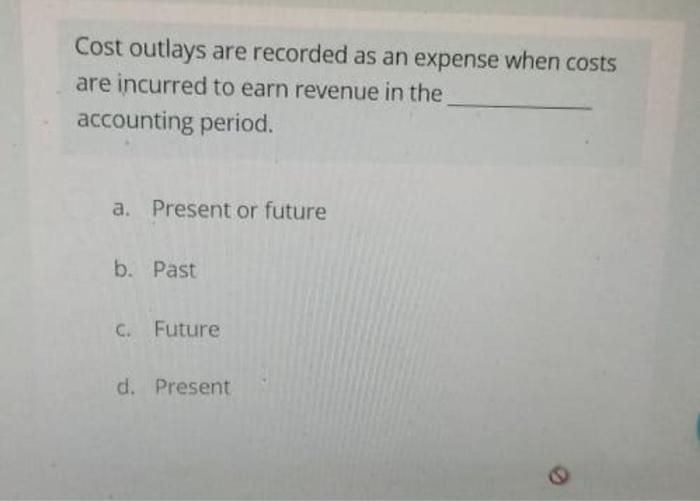

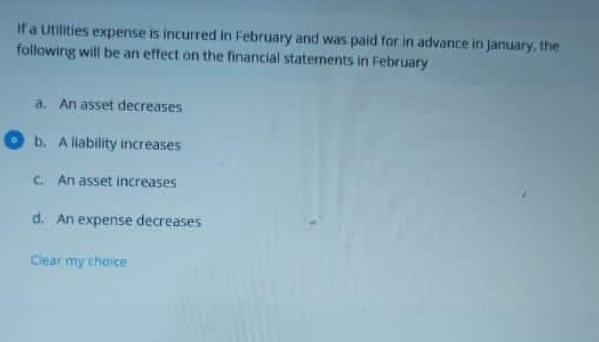

Cost outlays are recorded as an expense when costs are incurred to earn revenue in the accounting period. a. Present or future b. Past C.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Role Of Internal Auditing In A Federal Educational Institution Management Support And Decision Making Aid

Authors: Leonardo Gonçalves

1st Edition

6205061759, 978-6205061756