Answered step by step

Verified Expert Solution

Question

1 Approved Answer

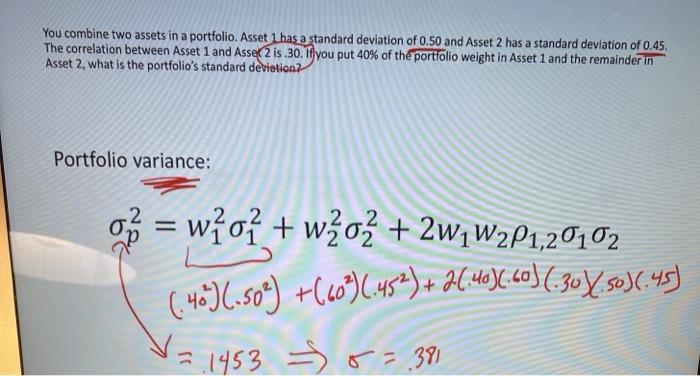

could someone show me how to work this problem in excel? please includw cell references and formulas You combine two assets in a portfolio. Asset

could someone show me how to work this problem in excel? please includw cell references and formulas

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance for Non Financial Managers

Authors: Pierre Bergeron

7th edition

176530835, 978-0176530839