Answered step by step

Verified Expert Solution

Question

1 Approved Answer

could you please help me? 1. Suppose the 1-year risk-free rate of return in the USA is 4.5%. The current exchange rate is 1 Pound

could you please help me?

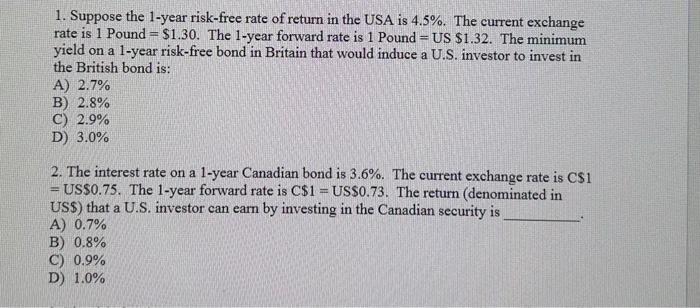

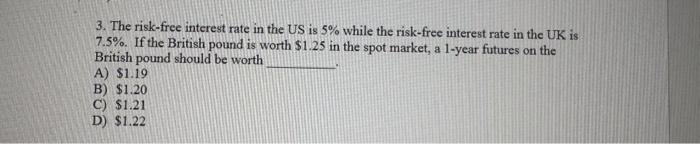

1. Suppose the 1-year risk-free rate of return in the USA is 4.5%. The current exchange rate is 1 Pound =$1.30. The 1 -year forward rate is 1 Pound = US $1.32. The minimum yield on a 1-year risk-free bond in Britain that would induce a U.S. investor to invest in the British bond is: A) 2.7% B) 2.8% C) 2.9% D) 3.0% 2. The interest rate on a 1 -year Canadian bond is 3.6%. The current exchange rate is CS1 = US\$0.75. The 1-year forward rate is C $1= US\$0.73. The return (denominated in US\$) that a U.S. investor can earn by investing in the Canadian security is A) 0.7% B) 0.8% C) 0.9% D) 1.0% 3. The risk-free interest rate in the US is 5% while the risk-free interest rate in the UK is 7.5%. If the British pound is worth $1.25 in the spot market, a 1-year futures on the British pound should be worth A) $1.19 B) $1.20 C) $1.21 D) $1.22 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Critical Handbook Of Money Laundering Policy Analysis And Myths

Authors: Petrus C. Van Duyne, Jackie H. Harvey, Liliya Y. Gelemerova

1st Edition

1137523972, 978-1137523976