Answered step by step

Verified Expert Solution

Question

1 Approved Answer

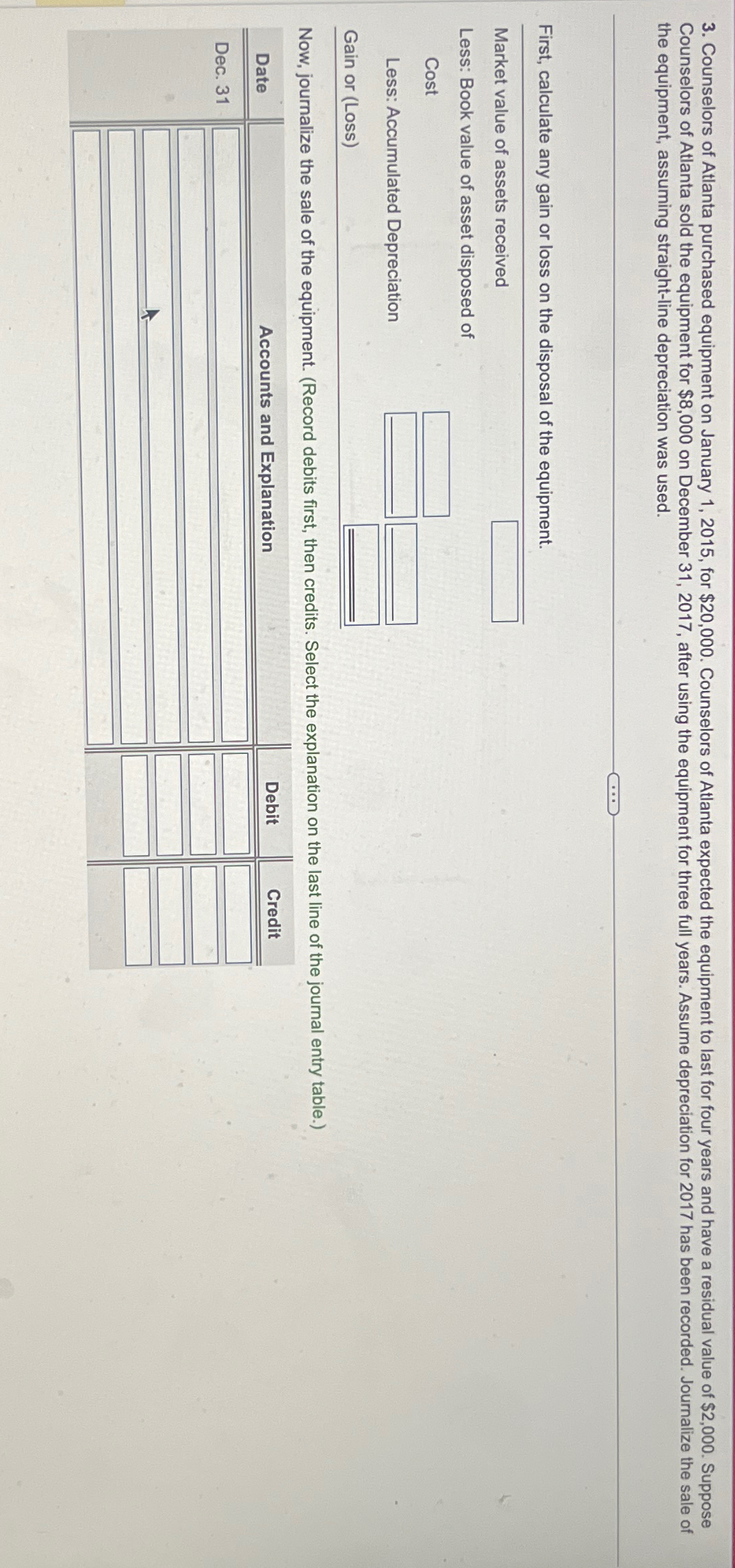

Counselors of Atlanta purchased equipment on January 1 , 2 0 1 5 , for $ 2 0 , 0 0 0 . Counselors of

Counselors of Atlanta purchased equipment on January for $ Counselors of Atlanta expected the equipment to last for four years and have a residual value of $ Suppose Counselors of Atlanta sold the equipment for $ on December after using the equipment for three full years. Assume depreciation for has been recorded. Journalize the sale of the equipment, assuming straightline depreciation was used.

First, calculate any gain or loss on the disposal of the equipment.

Market value of assets received

Less: Book value of asset disposed of

Cost

Less: Accumulated Depreciation

Gain or Loss

Now, journalize the sale of the equipment. Record debits first, then credits. Select the explanation on the last line of the journal entry table.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing A Modern Approach

Authors: Sanjay Basotia

1st Edition

938092903X, 978-9380929033