Answered step by step

Verified Expert Solution

Question

1 Approved Answer

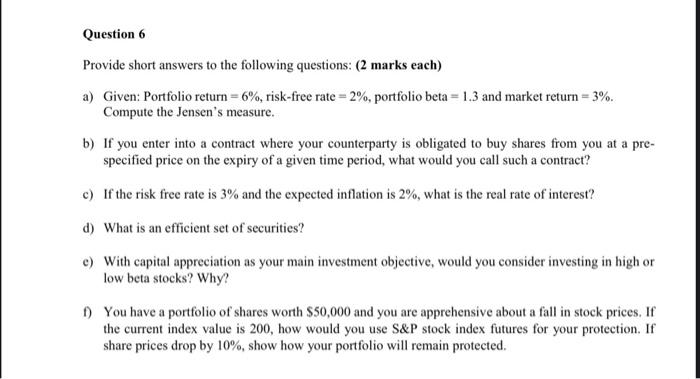

Course: MGMT3050 Investment & Analysis Please answer all parts Question 6 Provide short answers to the following questions: (2 marks each) a) Given: Portfolio return

Course: MGMT3050 Investment & Analysis

Question 6 Provide short answers to the following questions: (2 marks each) a) Given: Portfolio return = 6%, risk-free rate = 2%, portfolio beta = 1.3 and market return = 3%. Compute the Jensen's measure. b) If you enter into a contract where your counterparty is obligated to buy shares from you at a pre- specified price on the expiry of a given time period, what would you call such a contract? c) If the risk free rate is 3% and the expected inflation is 2%, what is the real rate of interest? d) What is an efficient set of securities? c) With capital appreciation as your main investment objective, would you consider investing in high or low beta stocks? Why? 1) You have a portfolio of shares worth $50,000 and you are apprehensive about a fall in stock prices. If the current index value is 200, how would you use S&P stock index futures for your protection. If share prices drop by 10%, show how your portfolio will remain protected Please answer all parts

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Institutions In Trade And Finance

Authors: Alasdair I. MacBean, P. N. Snowden

1st Edition

0043820336, 9780043820339