Answered step by step

Verified Expert Solution

Question

1 Approved Answer

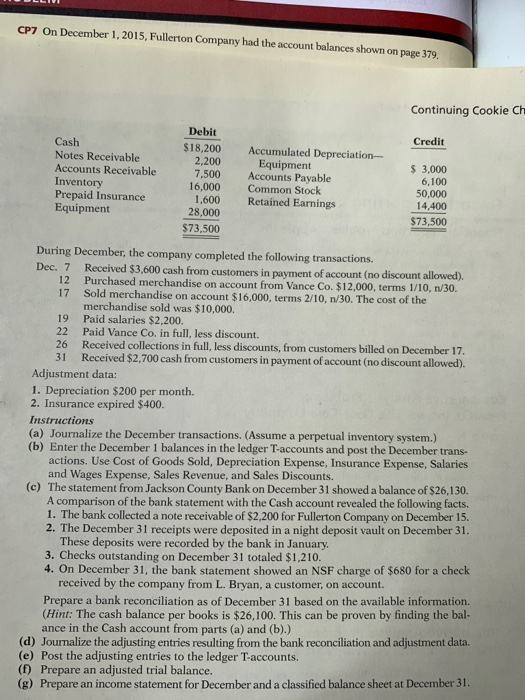

CP7 On December 1, 2015, Fullerton Company had the account balances shown on page 379. Continuing Cookie CH Credit Cash Notes Receivable Accounts Receivable Inventory

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Social Responsibility Audit A Management Tool For Survival

Authors: John W Humble

1st Edition

0900853522, 978-0900853524