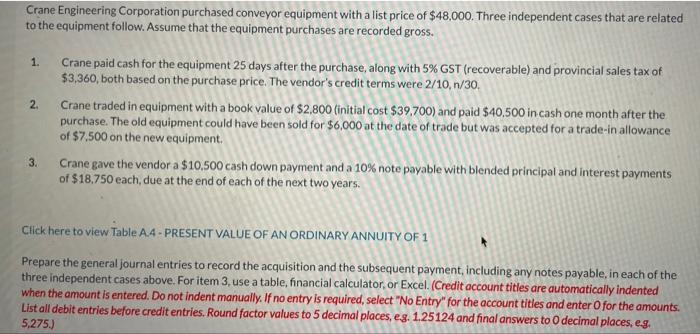

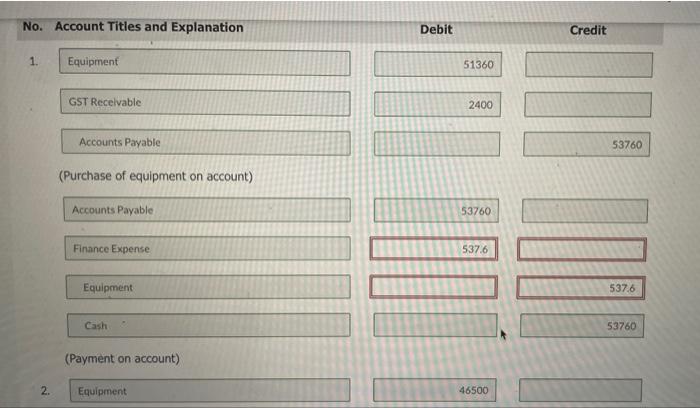

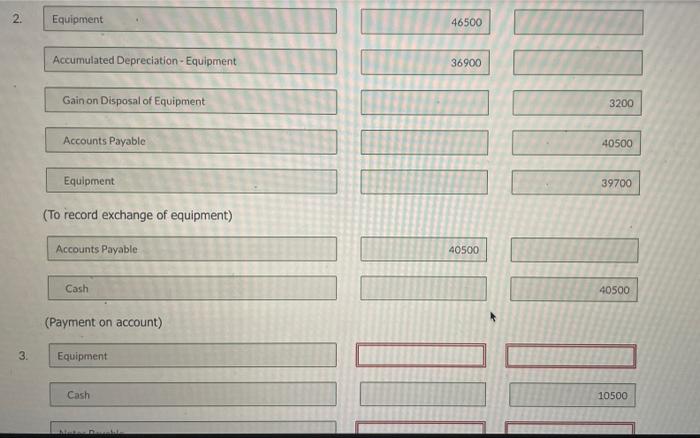

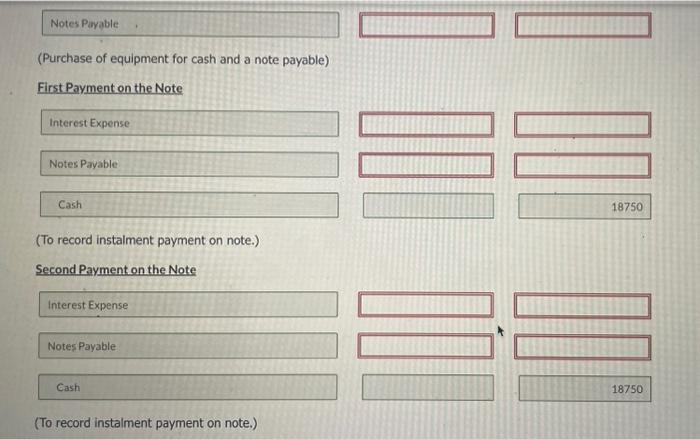

Crane Engineering Corporation purchased conveyor equipment with a list price of $48,000. Three independent cases that are related to the equipment follow. Assume that the equipment purchases are recorded gross. 1. Crane paid cash for the equipment 25 days after the purchase, along with 5% GST (recoverable) and provincial sales tax of $3,360, both based on the purchase price. The vendor's credit terms were 2/10,n/30. 2. Crane traded in equipment with a book value of $2,800 (initial cost $39,700 ) and paid $40,500 in cash one month after the purchase. The old equipment could have been sold for $6,000 at the date of trade but was accepted for a trade-in allowance of $7,500 on the new equipment. 3. Crane gave the vendor a $10,500 cash down payment and a 10% note payable with blended principal and interest payments of $18,750 each, due at the end of each of the next two years. Cilck here to view Table A.4 - PRESENT VALUE OF AN ORDINARY ANNUITY OF 1 Prepare the general journal entries to record the acquisition and the subsequent payment, including any notes payable, in each of the three independent cases above. For item 3, use a table, financial calculator, or Excel. (Credit account titles are outomatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts. List all debit entries before credit entries. Round factor values to 5 decimal places, e.g. 1.25124 and final answers to 0 decimal places, e.g. 5,275. No. Account Titles and Explanation 1. \begin{tabular}{|l|} \hline Equipment \\ \hline GST Recelvable \\ Accounts Payable \\ \hline \end{tabular} (Purchase of equipment on account) Accounts Payable Finance Expense Equipment Cash (Payment on account) 2. Equipment Debit Credit \begin{tabular}{|r|} \hline \\ \hline \\ \hline \\ \hline \\ \hline \end{tabular} \begin{tabular}{r} 53760 \\ \hline+5 \\ \hline \end{tabular} \begin{tabular}{|l|l|} \hline 1113760 \\ \hline \end{tabular} \begin{tabular}{|c|} \hline \multirow{8}{*}{} \\ \hline \\ \hline \\ \hline \\ \hline \\ \hline \\ \hline \\ \hline \\ \hline \end{tabular} 537.6 \begin{tabular}{|r|} \hline \\ \hline \\ \hline \\ \hline 53760 \\ \hline \end{tabular} 46500 2. Equipment Accumulated Depreciation-Equipment Gain on Disposal of Equipment Accounts Payable Equipment (To record exchange of equipment) Accounts Payable 40500 Cash (Payment on account) 3. Equipment Cash 10500 Notes Payable (Purchase of equipment for cash and a note payable) First Payment on the Note Interest Expense Notes Payable Cash (To record instalment payment on note.) Second Payment on the Note Interest Expense Notes Payable Cash (To record instalment payment on note.)