Question

Create the statement of the problem in a good and long paragraph. not good is downvoted. Create the statement of the problem. Create the statement

Create the statement of the problem in a good and long paragraph. not good is downvoted. Create the statement of the problem. Create the statement of the problem.

Create the statement of the problem.

Create the statement of the problem about save mart company with 20 sentences, minimum. should have 700 words.

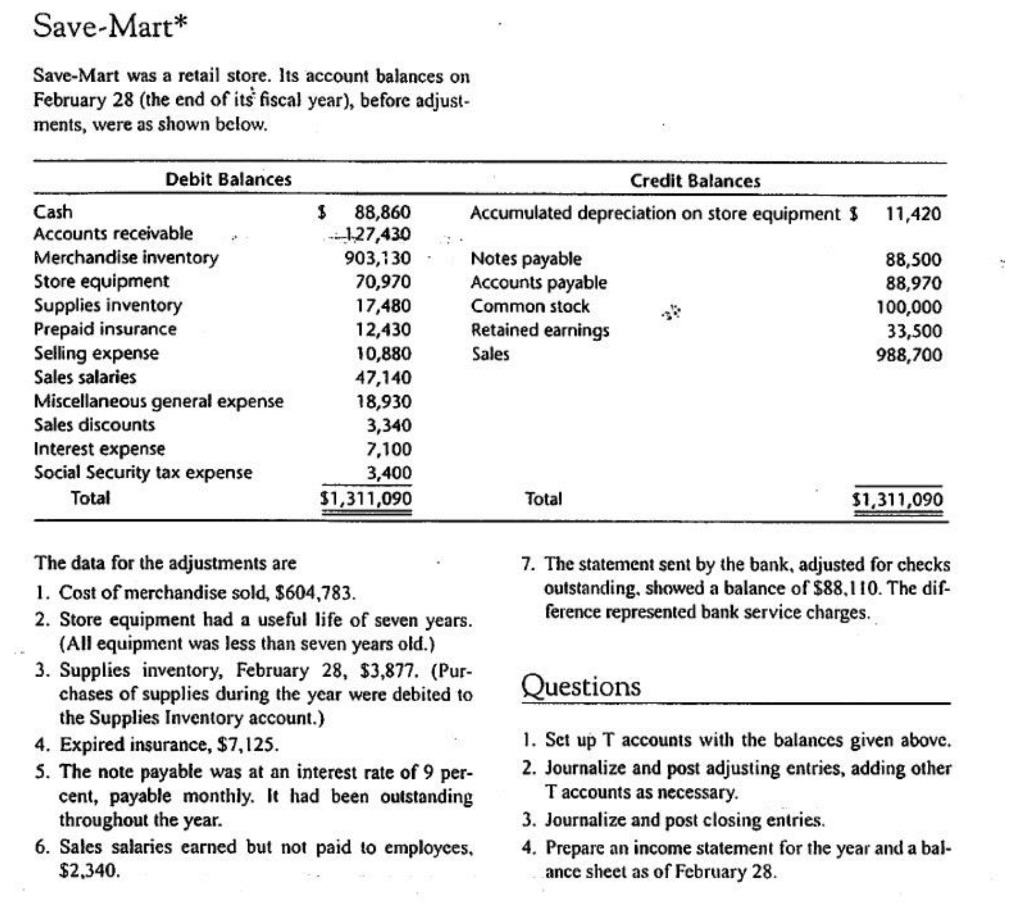

Save-Mart* Save-Mart was a retail store. Its account balances on February 28 (the end of its fiscal year), before adjust- ments, were as shown below. Debit Balances Credit Balances Accumulated depreciation on store equipments 11,420 Cash Accounts receivable Merchandise inventory Store equipment Supplies inventory Prepaid insurance Selling expense Sales salaries Miscellaneous general expense Sales discounts Interest expense Social Security tax expense Total $ 88,860 127,430 903,130 70,970 17,480 12,430 10,880 47,140 18,930 3,340 7,100 3,400 $1,311,090 Notes payable Accounts payable Common stock Retained earnings Sales 88,500 88,970 100,000 33,500 988,700 Total $1,311,090 7. The statement sent by the bank, adjusted for checks outstanding, showed a balance of $88,110. The dif- ference represented bank service charges. Questions The data for the adjustments are 1. Cost of merchandise sold, $604,783. 2. Store equipment had a useful life of seven years. (All equipment was less than seven years old.) 3. Supplies inventory, February 28, $3,877. (Pur- chases of supplies during the year were debited to the Supplies Inventory account.) 4. Expired insurance, $7,125. 5. The note payable was at an interest rate of 9 per- cent, payable monthly. It had been outstanding throughout the year. 6. Sales salaries earned but not paid to employees, $2,340. 1. Set up T accounts with the balances given above. 2. Journalize and post adjusting entries, adding other T accounts as necessary. 3. Journalize and post closing entries. 4. Prepare an income statement for the year and a bal- ance sheet as of February 28Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

E Commerce Operational Aspects Accounting Auditing And Taxation Issues

Authors: Lata Sharma

1st Edition

8177084097, 978-8177084092