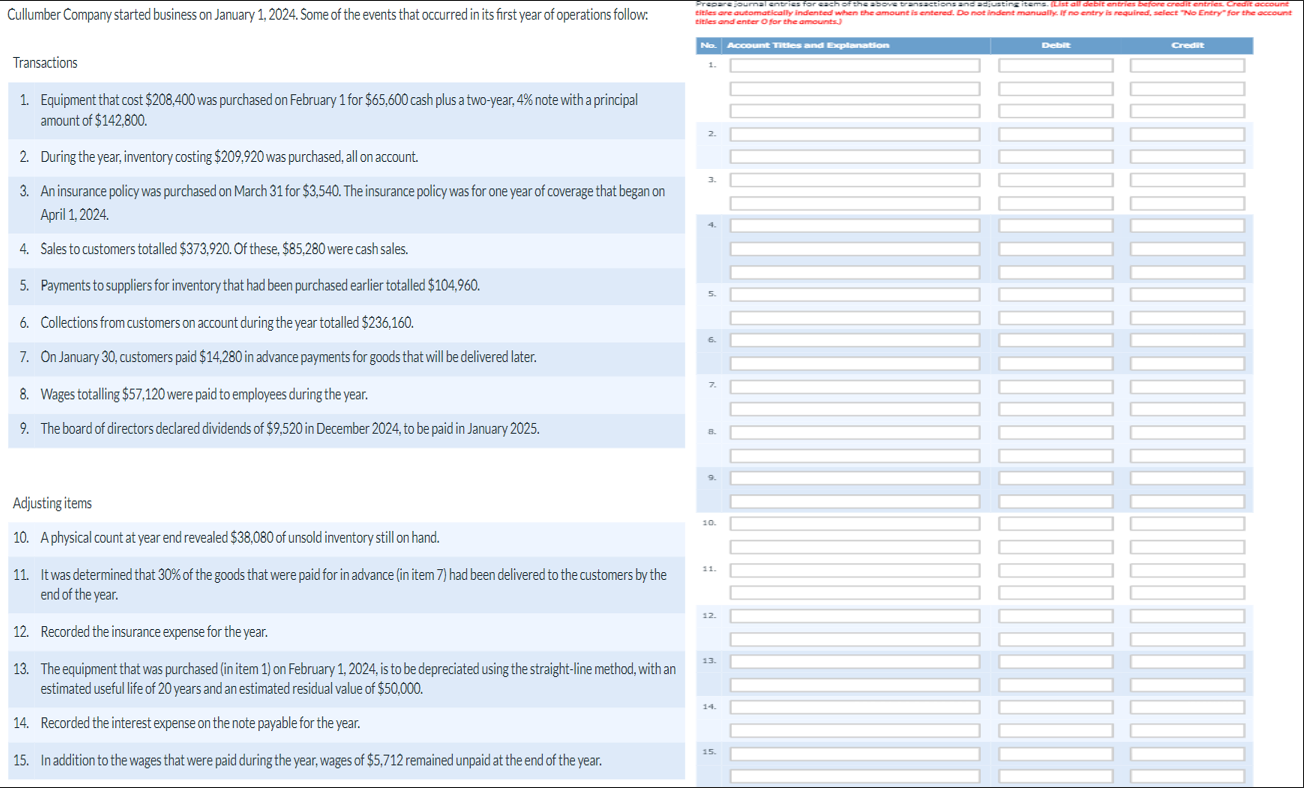

Cullumber Company started business on January 1, 2024. Some of the events that occurred in its first year of operations follow: Transactions 1. Equipment

Cullumber Company started business on January 1, 2024. Some of the events that occurred in its first year of operations follow: Transactions 1. Equipment that cost $208,400 was purchased on February 1 for $65,600 cash plus a two-year, 4% note with a principal amount of $142,800. 2. During the year, inventory costing $209,920 was purchased, all on account. 3. An insurance policy was purchased on March 31 for $3,540. The insurance policy was for one year of coverage that began on April 1, 2024. 4. Sales to customers totalled $373,920. Of these, $85,280 were cash sales. 5. Payments to suppliers for inventory that had been purchased earlier totalled $104,960. 6. Collections from customers on account during the year totalled $236,160. 7. On January 30, customers paid $14,280 in advance payments for goods that will be delivered later. 8. Wages totalling $57,120 were paid to employees during the year. 9. The board of directors declared dividends of $9,520 in December 2024, to be paid in January 2025. Prepare journal entries for each of the above transactions and adjusting items. (List all debit entries before credit entries. Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts.) No. Account Titles and Explanation 2. 6. Debit Credit Adjusting items 10. A physical count at year end revealed $38,080 of unsold inventory still on hand. 11. It was determined that 30% of the goods that were paid for in advance (in item 7) had been delivered to the customers by the end of the year. 12. Recorded the insurance expense for the year. 13. The equipment that was purchased (in item 1) on February 1, 2024, is to be depreciated using the straight-line method, with an estimated useful life of 20 years and an estimated residual value of $50,000. 14. Recorded the interest expense on the note payable for the year. 10. 14. 15. 15. In addition to the wages that were paid during the year, wages of $5,712 remained unpaid at the end of the year.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Here are the answers for the Cullumber Company transactions and adjusting items Transactions 1 Equip...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Christopher D. Burnley

2nd Canadian Edition

1119406927, 978-1119406921