Question

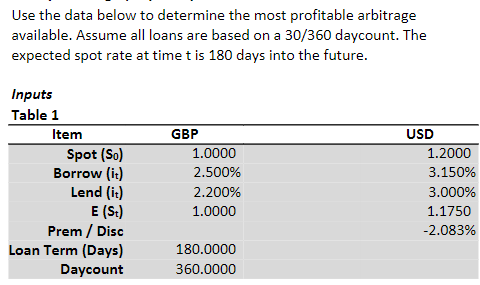

Currency Arbitrage Use the data below to determine the most profitable arbitrage available. Assume all loans are based on a 30/360 daycount. The expected spot

Currency Arbitrage Use the data below to determine the most profitable arbitrage available. Assume all loans are based on a 30/360 daycount. The expected spot rate at time t is 180 days into the future. Inputs Table 1 Item GBP USD Spot (S0) 1.0000 1.2000 Borrow (it) 2.500% 3.150% Lend (it) 2.200% 3.000% E (St) 1.0000 1.1750 Prem / Disc -2.083% Loan Term (Days) 180.0000 Daycount 360.0000

Please show work

Use the data below to determine the most profitable arbitrage available. Assume all loans are based on a 30/360 daycount. The expected spot rate at time t is 180 days into the futureStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Executive Finance And Strategy

Authors: Ralph Tiffin

1st Edition

0749471506, 978-0749471507