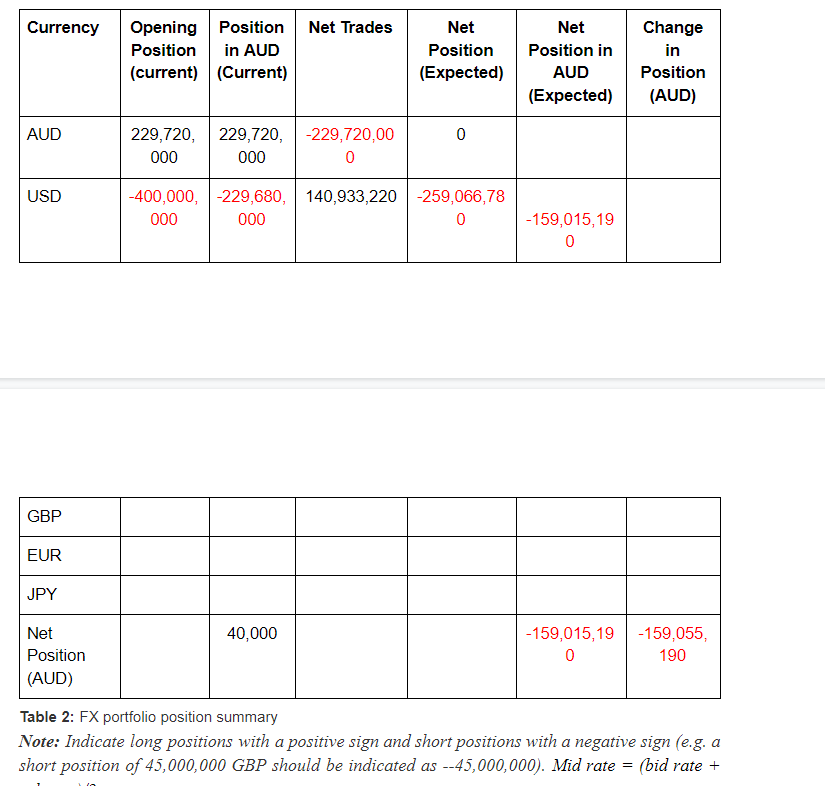

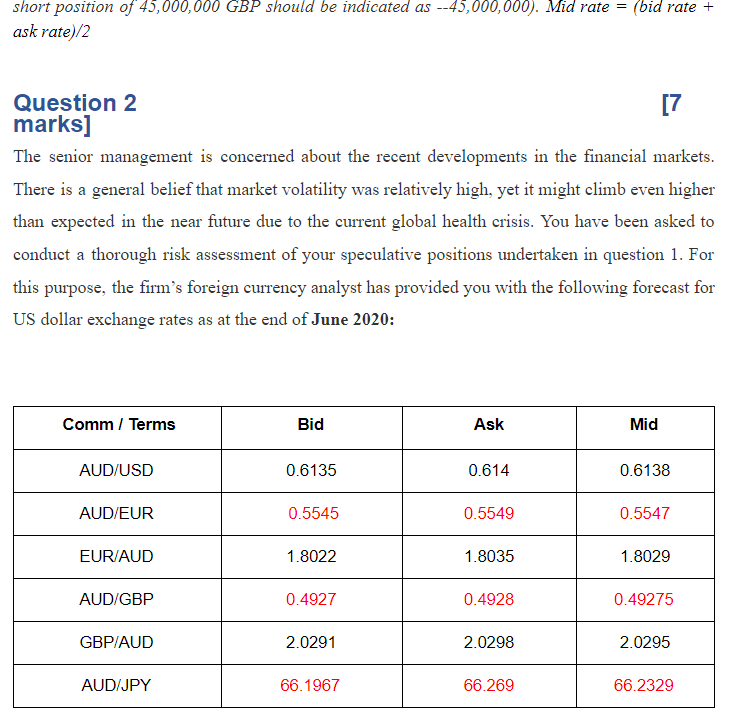

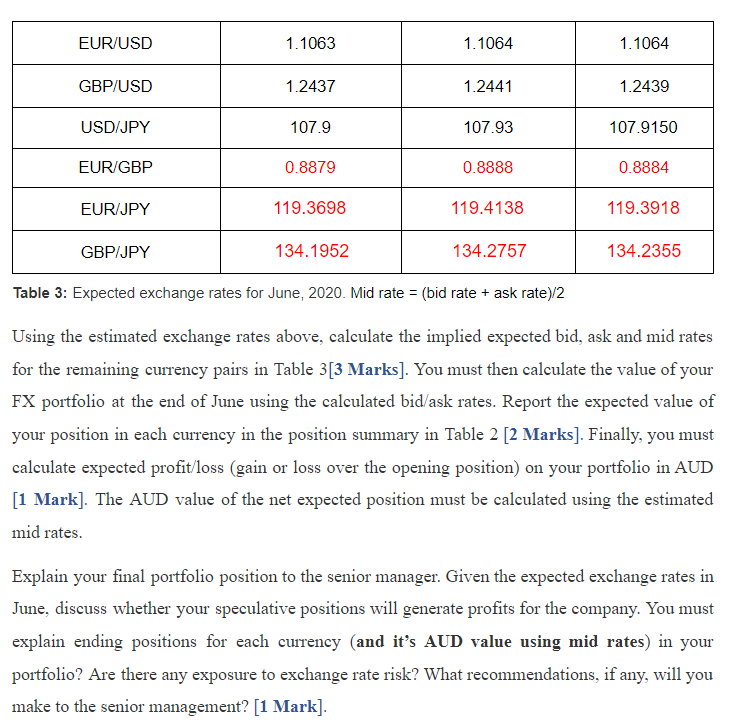

Currency Net Trades Opening Position Position in AUD (current) (Current) Net Position (Expected) Net Position in AUD (Expected) Change in Position (AUD) AUD 0 229,720, 229,720, 000 000 -229,720,00 0 USD -400,000, -229,680, 140,933,220 -259,066,78 000 000 0 -159,015,19 0 GBP EUR JPY 40,000 Net Position (AUD) -159,015,19-159,055, 0 190 Table 2: FX portfolio position summary Note: Indicate long positions with a positive sign and short positions with a negative sign (e.g. a short position of 45,000,000 GBP should be indicated as --45,000,000). Mid rate = (bid rate + short position of 45,000,000 GBP should be indicated as --45,000,000). Mid rate = (bid rate + ask rate)/2 Question 2 [7 marks] The senior management is concerned about the recent developments in the financial markets. There is a general belief that market volatility was relatively high, yet it might climb even higher than expected in the near future due to the current global health crisis. You have been asked to conduct a thorough risk assessment of your speculative positions undertaken in question 1. For this purpose, the firm's foreign currency analyst has provided you with the following forecast for US dollar exchange rates as at the end of June 2020: Comm / Terms Bid Ask Mid AUD/USD 0.6135 0.614 0.6138 AUD/EUR 0.5545 0.5549 0.5547 EUR/AUD 1.8022 1.8035 1.8029 AUD/GBP 0.4927 0.4928 0.49275 GBP/AUD 2.0291 2.0298 2.0295 AUD/JPY 66.1967 66.269 66.2329 EUR/USD 1.1063 1.1064 1.1064 GBP/USD 1.2437 1.2441 1.2439 USD/JPY 107.9 107.93 107.9150 EUR/GBP 0.8879 0.8888 0.8884 EUR/JPY 119.3698 119.4138 119.3918 GBP/JPY 134.1952 134.2757 134.2355 Table 3: Expected exchange rates for June, 2020. Mid rate = (bid rate + ask rate)/2 Using the estimated exchange rates above, calculate the implied expected bid, ask and mid rates for the remaining currency pairs in Table 3[3 Marks]. You must then calculate the value of your FX portfolio at the end of June using the calculated bid/ask rates. Report the expected value of your position in each currency in the position summary in Table 2 [2 Marks]. Finally, you must calculate expected profit/loss (gain or loss over the opening position) on your portfolio in AUD [1 Mark]. The AUD value of the net expected position must be calculated using the estimated mid rates. Explain your final portfolio position to the senior manager. Given the expected exchange rates in June, discuss whether your speculative positions will generate profits for the company. You must explain ending positions for each currency (and it's AUD value using mid rates) in your portfolio? Are there any exposure to exchange rate risk? What recommendations, if any, will you make to the senior management? [1 Mark]. Currency Net Trades Opening Position Position in AUD (current) (Current) Net Position (Expected) Net Position in AUD (Expected) Change in Position (AUD) AUD 0 229,720, 229,720, 000 000 -229,720,00 0 USD -400,000, -229,680, 140,933,220 -259,066,78 000 000 0 -159,015,19 0 GBP EUR JPY 40,000 Net Position (AUD) -159,015,19-159,055, 0 190 Table 2: FX portfolio position summary Note: Indicate long positions with a positive sign and short positions with a negative sign (e.g. a short position of 45,000,000 GBP should be indicated as --45,000,000). Mid rate = (bid rate + short position of 45,000,000 GBP should be indicated as --45,000,000). Mid rate = (bid rate + ask rate)/2 Question 2 [7 marks] The senior management is concerned about the recent developments in the financial markets. There is a general belief that market volatility was relatively high, yet it might climb even higher than expected in the near future due to the current global health crisis. You have been asked to conduct a thorough risk assessment of your speculative positions undertaken in question 1. For this purpose, the firm's foreign currency analyst has provided you with the following forecast for US dollar exchange rates as at the end of June 2020: Comm / Terms Bid Ask Mid AUD/USD 0.6135 0.614 0.6138 AUD/EUR 0.5545 0.5549 0.5547 EUR/AUD 1.8022 1.8035 1.8029 AUD/GBP 0.4927 0.4928 0.49275 GBP/AUD 2.0291 2.0298 2.0295 AUD/JPY 66.1967 66.269 66.2329 EUR/USD 1.1063 1.1064 1.1064 GBP/USD 1.2437 1.2441 1.2439 USD/JPY 107.9 107.93 107.9150 EUR/GBP 0.8879 0.8888 0.8884 EUR/JPY 119.3698 119.4138 119.3918 GBP/JPY 134.1952 134.2757 134.2355 Table 3: Expected exchange rates for June, 2020. Mid rate = (bid rate + ask rate)/2 Using the estimated exchange rates above, calculate the implied expected bid, ask and mid rates for the remaining currency pairs in Table 3[3 Marks]. You must then calculate the value of your FX portfolio at the end of June using the calculated bid/ask rates. Report the expected value of your position in each currency in the position summary in Table 2 [2 Marks]. Finally, you must calculate expected profit/loss (gain or loss over the opening position) on your portfolio in AUD [1 Mark]. The AUD value of the net expected position must be calculated using the estimated mid rates. Explain your final portfolio position to the senior manager. Given the expected exchange rates in June, discuss whether your speculative positions will generate profits for the company. You must explain ending positions for each currency (and it's AUD value using mid rates) in your portfolio? Are there any exposure to exchange rate risk? What recommendations, if any, will you make to the senior management? [1 Mark]