Answered step by step

Verified Expert Solution

Question

1 Approved Answer

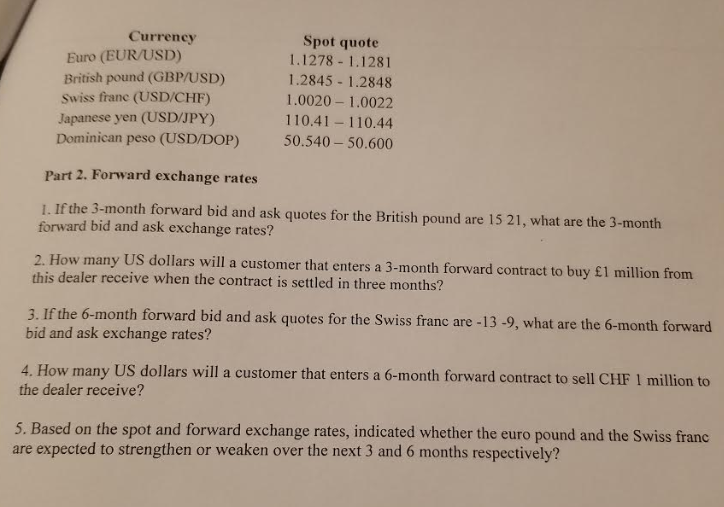

Currency Spot quote 1.1278 - 1.1281 1.2845 1.2848 1.0020-1.0022 110.41-110.44 Euro (EUR/USD) British pound (GBP/USD) Swiss franc (USD/CHF) Japanese yen (USD/JPY) Dominican peso (USD/DOP) 50.540-

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bankers Handbook On Credit Management

Authors: Indian Institute Of Banking & Finance

1st Edition

9387957853, 978-9387957855