Answered step by step

Verified Expert Solution

Question

1 Approved Answer

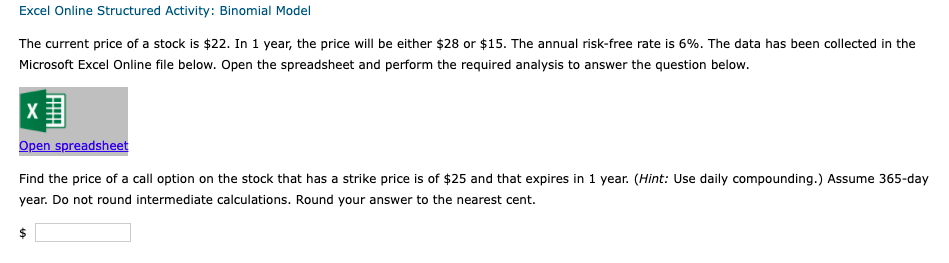

Current price $22.00 High price, Year 1 $28.00 Low price, Year 1 $15.00 Risk-free rate, r RF 6.00% Strike price $25.00 Time until expiration (in

| Current price | $22.00 | ||||

| High price, Year 1 | $28.00 | ||||

| Low price, Year 1 | $15.00 | ||||

| Risk-free rate, rRF | 6.00% | ||||

| Strike price | $25.00 | ||||

| Time until expiration (in years) | 1.00 | ||||

| Number of days per year | 365 | ||||

| Outcome | Stock Price | Strike Price | Option Payoff | ||

| Price up | $28.00 | $25.00 | $3.00 | ||

| Price down | $15.00 | $25.00 | $0.00 | ||

| Range | $13.00 | $3.00 | |||

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started